How to Read an Apportionment, Part II: Program Controls and Legal Weight

The difference between an accounting note and a criminal referral often comes down to a single letter. In Part II, we look at why 'A' footnotes carry the weight of the law—and why a $1 mistake can trigger a federal investigation.

1. What is an apportionment?

2. How to Read an Apportionment, Part I: Structure and Time-Based Controls

3. How to Read an Apportionment, Part II: Program Controls and Legal Weight

In Part I, we covered the structure of an apportionment and how OMB controls timing through Category A (quarterly) and Category C (future years).

But timing isn't OMB's only lever. They can also control which programs get funding—and that's where the legal stakes get interesting.

The 60-Second Version

| Apportionment Category | Controls |

|---|---|

| Category A | Time period (quarterly) |

| Category B | Program/project/activity |

| Category C | Future fiscal years |

| Category AB | Both time AND program |

Apportionments have two halves:

| Section | What It Shows |

|---|---|

| Budgetary Resources (top half, 1XXX lines) | Where the money comes from |

| Application of Budgetary Resources (bottom half, 6XXX lines) | How it's allocated |

Apportionment footnotes apply to a specific section. Where they are applied has different legal effect.

| Type | Section | What It Shows | Legally Binding? |

|---|---|---|---|

| B | Budgetary Resources | Information about funding sources | No |

| A | Application of Budgetary Resources | Direction on the use of funds | Yes |

Check out our quick visual explainer.

The Key Distinction:

Categorical apportionments and A footnotes = Hard limit. Exceed these, and you've violated the Anti-Deficiency Act. Responsible officers face disciplinary action or criminal referral and could face fines or jail time.

B footnotes = Informational. OMB's documentation on how money came into or out of the account. No criminal exposure.

A note of caution:

Apportionment categories are not the same as footnote types. Other than B apportionment footnotes, all apportionment lines and footnotes have the force of law.

Program-Based Apportionments: Category B

Category B distributes funds by program, project, or activity—not time.

How It Works

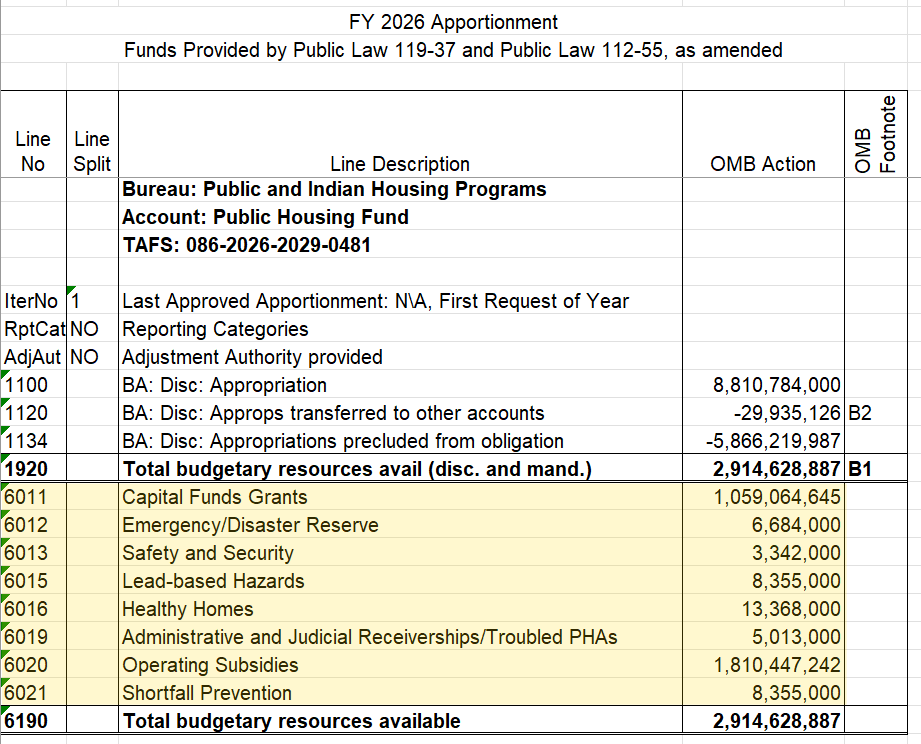

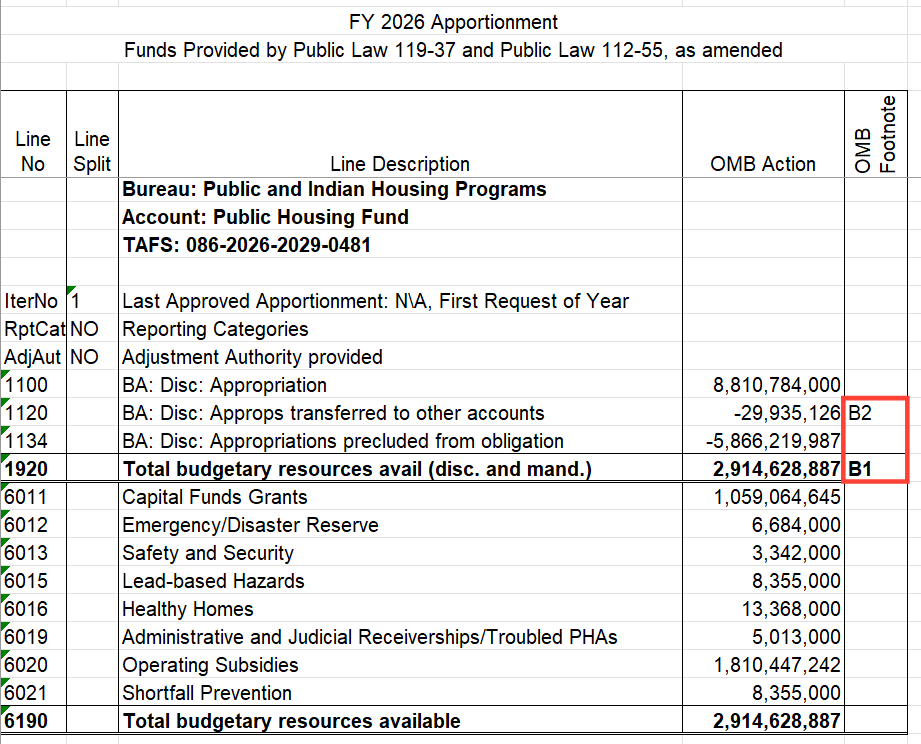

Instead of (or in addition to) quarterly amounts, OMB allocates to specific purposes. Take HUD's Public Housing Fund-a sprawling appropriation with six numbered sub-paragraphs and different purposes:

Source: OMB | OpenOMB.org

Let's look at what's going on in this apportionment. First, the top half (lines 1XXX). The appropriation is contained in the CR. OMB has made the pro rata share calculation (33.42 percent of $8.8 billion) and reduced the budget authority available for obligation on line 1134. There's also a transfer of funds out of the account on line 1120. There's also a footnote, B2, that explains what is happening with this transfer-we'll come back to this later. All told, this account has $2.9 billion available right now, shown in line 1920.

The underlying appropriation for this account starts like this:

For 2024 payments to public housing agencies for the operation and management of public housing..., $8,810,784,000, to remain available until September 30, 2027:

It then goes on:

Provided, That of the sums appropriated under this heading—

(1) $5,475,784,000 shall be available for the Secretary to allocate pursuant to the Operating Fund formula...

(2) $25,000,000 shall be available for the Secretary to allocate pursuant to a need-based application process...for financial shortfalls...

(3) $3,200,000,000 shall be available for the Secretary to allocate pursuant to the Capital Fund formula...

This appropriation isn't just one big appropriation. It's one big appropriation for multiple things with different purposes. In order to operationalize this statutory direction, OMB needs to utilize apportionments by project, program or activity, or Category B apportionments. Now, let's turn our attention to the bottom half:

| Line | Program/Activity | Apportioned |

|---|---|---|

| 6011 | Capital Funds Grants | $1,059,064,645 |

| 6012 | Emergency/Disaster Reserve | $6,684,000 |

| 6013 | Safety and Security | $3,342,000 |

| 6015 | Lead-based Hazards | $8,355,000 |

| 6016 | Healthy Homes | $13,368,000 |

| 6019 | Administrative and Judicial Receiverships/Troubled PHAs | $5,013,000 |

| 6020 | Operating Subsidies | $1,810,447,242 |

| 6021 | Shortfall Prevention | $8,355,000 |

| 6190 | Total | $2,914,628,887 |

In these lines, OMB has given each of the purpose-specific appropriations in the Public Housing Fund their own pro rata amount for the CR period. You can see how the lines in the apportionment map back to a specific paragraph in the appropriations text.

| Apportionment Line | Appropriation Paragraph |

|---|---|

| 6011 Capital Funds | (3) Capital Fund formula |

| 6020 Operating Subsidies | (1) Operating Fund formula |

| 6021 Shortfall Prevention | (2) need-based application |

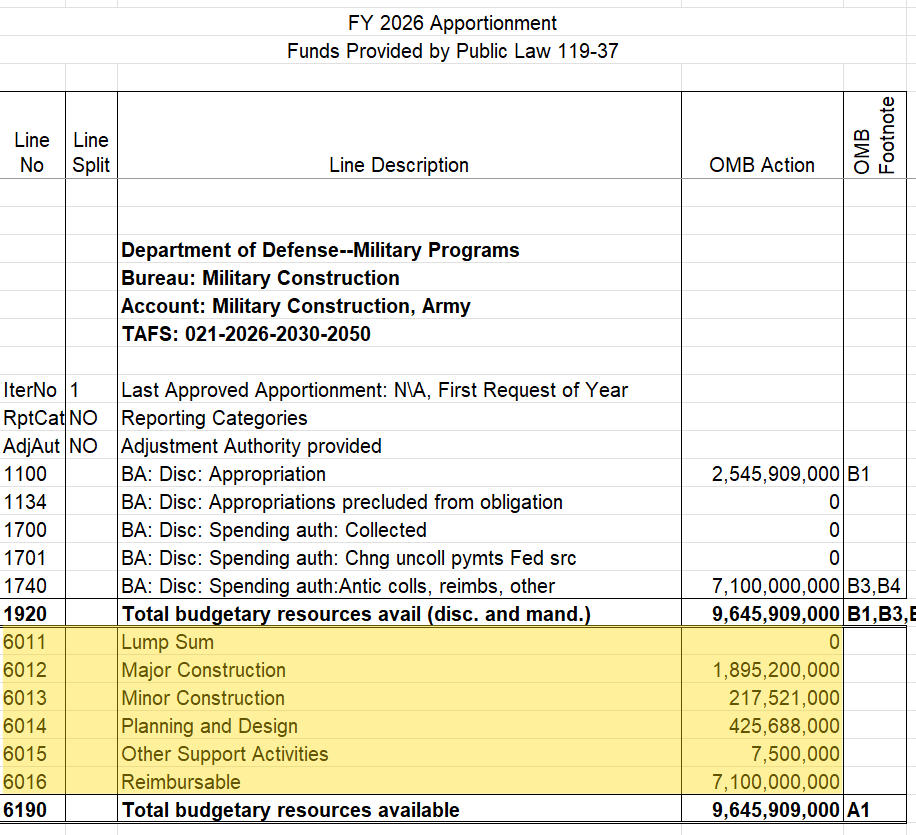

While the Public Housing Fund apportionment lines closely follow the appropriations text, that's not always the case. Consider this apportionment for Army, Military Construction:

Source: OMB | OpenOMB.org

While not the focus of this post, note line 1740: $7.1 billion for anticipated reimbursable activities. In an effort to economize, Federal agencies often provide services to other agencies. In this case, the Army is going to construct facilities for another branch of the Department or for another agency. These funds need to be recorded and apportioned before the agency can incur obligations against those funds. That's what's happening here. As the reimbursements are collected in this account, OMB will reduce the anticipated reimbursements in line 1740 and move them to line 1700. OMB then apportions those funds on line 6016 in the bottom half.

In the bottom section, we have these lines:

| Line | Program/Activity | Apportioned |

|---|---|---|

| 6011 | Lump Sum | $0 |

| 6012 | Major Construction | $1,895,200,000 |

| 6013 | Minor Construction | $217,521,000 |

| 6014 | Planning and Design | $425,688,000 |

| 6015 | Other Support Activities | $7,500,000 |

| 6016 | Reimbursable | $7,100,000,000 |

| 6190 | Total | $9,645,909,000 |

While the statute provides some guidance on how these funds can be used, it's silent on the split between Major and Minor Construction, for example. In this apportionment, the agency has proposed and OMB has approved this particular split between the two categories. This is an example of OMB using a Category B apportionment to shape and manage the execution of appropriated funds in the absence of explicit Congressional direction.

Why Category B Exists

OMB uses program breakdowns to:

- Track spending against congressional intent

- Provide program-level visibility

- Signal administration priorities

Combined Categories

There are some times where a program requires apportionments by both time and project.

This is the tightest form of control. While it sounds complicated, OMB makes it simple, it's really just another line on the apportionment.

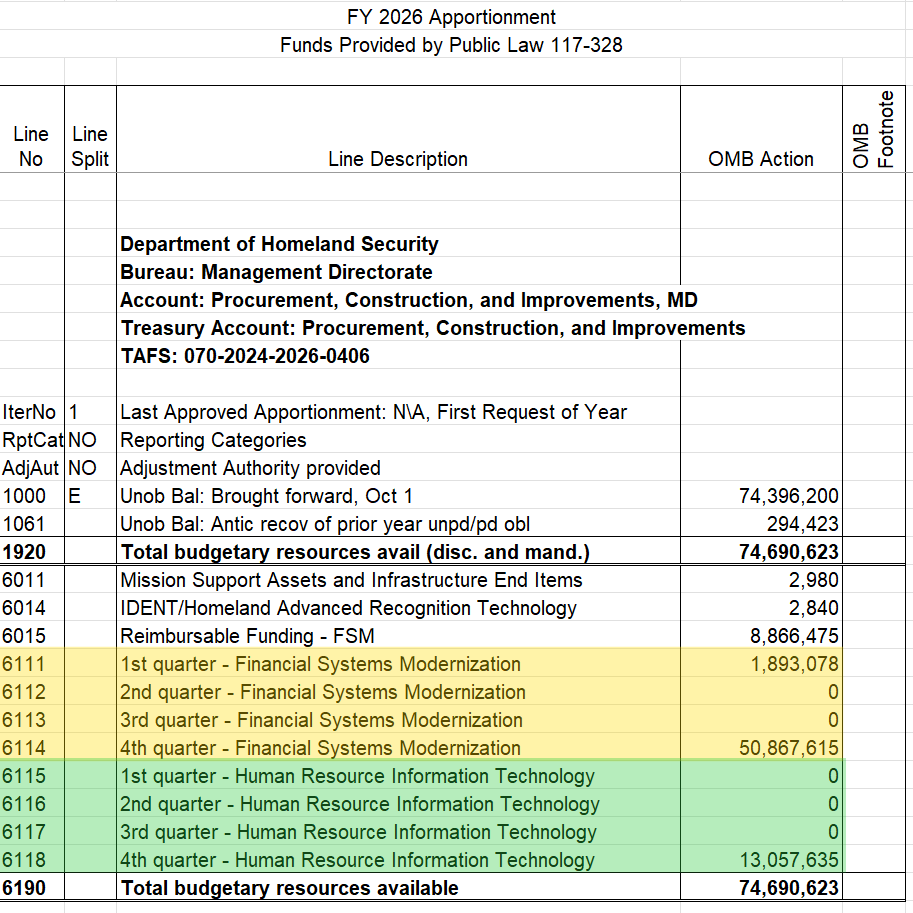

Here's an example:

Source: OMB | OpenOMB.org

This is the latest apportionment for DHS's Management Directorate's Procurement, Construction, and Improvements Account. If you look at lines 6111-6114 (Financial Systems Modernization) and lines 6115-6118 (Human Resource Information Technology), you'll see that these apportionment lines combine both quarter and activity. We call these AB apportionments.

Sometimes you'll see reservations for activities in a future fiscal year. Take the Center on Medicare and Medicaid Services, Program Management as an example. I'm not going to show it in full because it's a large apportionment document, but you'll see lines like:

| Line | Description | Amount |

|---|---|---|

| 6048 | Marketplace User Fees (Section 1311&1321, P.L.111-148) | $2,200,000,000 |

| 6170 | Apportioned in FY 2027 and future fiscal years - Marketplace User Fees (Section 1311&1321, P.L.111-148) | $1,315,152,321 |

Line 6048 is a category B apportionment for marketplace user fees, and available right now. Line 6170 is reserved for the same activity, but in a future fiscal year.

The combined categories aren't used frequently, but they do exist. They're just like any other line when it comes to their applicability.

Footnotes: The Fine Print

Beyond categories, apportionments often contain footnotes with specific restrictions. These matter.

B Footnotes: Budgetary Resources

First, let's talk about B footnotes. B footnotes do not have the force of law and provide a discussion of what's going on with the funding in an account. Take the Public Housing Fund from earlier in the post as an example: look at the right most column. You see B1 and B2 under the "OMB Footnote" column.

Source: OMB | OpenOMB.org

If you go to the "OMB Footnotes" tab of the Excel file for this apportionment or click the "Footnotes" button on OpenOMB.org, you'll see:

B1 Pursuant to the authority in OMB Circular A-11 section 120.21, one or more lines on the apportionment (including lines above line 1920) may have been rounded up and as such, those rounded lines will not match the actuals reported on the SF-133. HUD will ensure that its funds control system will only allot actuals.

B2 Pursuant to the transfer authority provided under the Rental Assistance Demonstration heading as authorized by the Consolidated and Furthering Continuing Appropriations Act, 2012 (P.L. 112-55), the amount of $22,784,814 is transferred to the TBRA account (86-0302) and $7,150,312 is transferred to the PBRA account (86-0303) for the purpose of Rental Assistance Demonstration (RAD) conversions.

B1 is by far the most common B footnote you'll see. Apportionments round to whole dollars, but the SF-133 reports in cents. This footnote reconciles the two reporting systems. While it might seem like an insignificant amount of money to be concerned about, literally less than $1, the Antideficiency Act (ADA) doesn't have a de minimus exception and there have been ADA cases about the difference in rounding. One penny of over-obligation is a violation.

Footnote B2 describes the sources and authorities used to transfer funds out of this account and notes where it's going. In this case, HUD is using the Rental Assistance Demonstration transfer authority to move money into the Tenant- and Project-Based Rental Assistance Accounts.

Apportionments apply to the lines they're next to, so B1 applies to Line 1920, and by extension all of the budgetary resources, and B2 applies to only Line 1120.

Other common B footnotes you'll encounter look like this:

The Contract Authority total (line 1600) represents an approximate projection of expected sales, based on historical data, since sales are continuously ongoing.

011-8242 /X - Foreign Military Sales Trust Fund, Sep. 30, 2025

These funds reflect anticipated collections from an interagency agreement with the Department of Education to conduct the 1776 Prize program.

381-8282 /2026 - James Madison Memorial Fellowship Trust Fund, Dec. 22, 2025

Pursuant to the transfer authority incorporated by Title I, Section 1101(a)(8) of the Full-Year Continuing Appropriations and Extensions Act, 2025, Pub. L. No. 119-4, which continues the transfer authority outlined in Division D, Title I, Section 106(b) of the Further Consolidated Appropriations Act, 2024, Pub. L. No. 118-47, this apportionment transfers $2,505,000 from the State Unemployment Insurance and Employment Service Operations account to the Program Administration (016-2025-2026-0172) account to support the operations, maintenance, and continued enhancement of the ETA grants management system in the HHS GrantSolutions platform. Of this amount, $1,940,000 will come from UI State Administration's RESEA activity, $516,000 will come from ES Grants to States, and $49,000 will come from Workforce Information.

016-0179 2025/2026 - State Unemployment Insurance and Employment Service Operations, Dec. 19, 2025

These all take a common form- they discuss specific estimates or transfers that affect the funding line that the footnote applies to. While the B footnote itself doesn't have the force of law, the line and the amount it applies to does.

A Footnotes: Application of Budgetary Resources

The other type of footnotes, A footnotes, apply to the bottom half of the apportionment and direct how the agency can use apportioned funds. A footnotes are legally binding and violating an A footnote is a violation of the Antideficiency Act.

Here's an example:

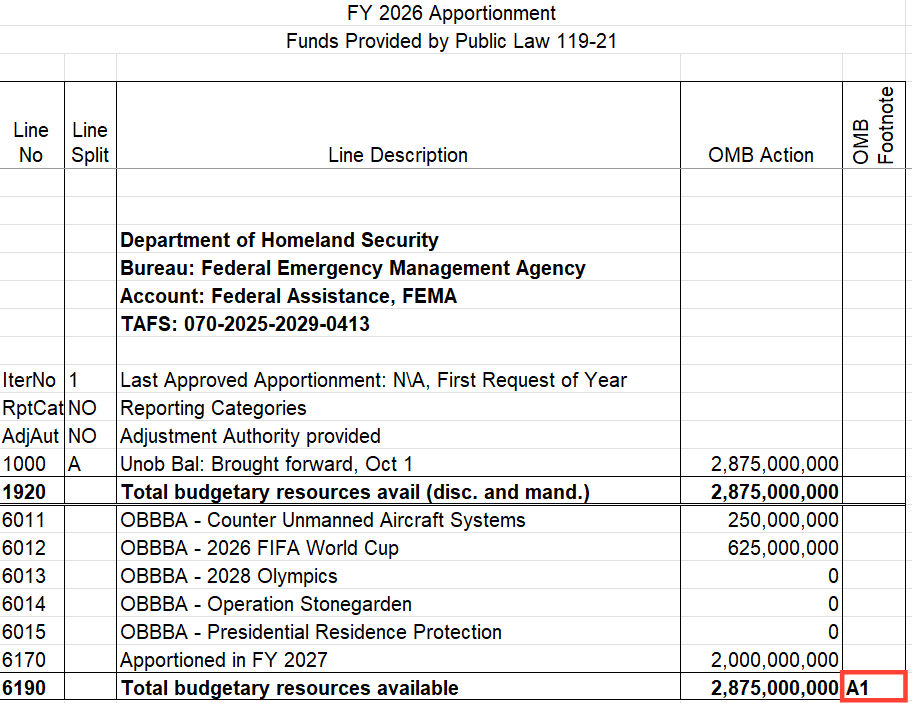

Source: OMB | OpenOMB.org

This is FEMA's Federal Assistance account for funds provided in the One Big Beautiful Bill Act (OBBBA). The top half is fairly routine-this account brought forward $2.875 billion from FY 2025 into FY2026. The Category B lines have allocated some of the resources, but $2 billion will be reserved for future years. You'll note that line 6190 has an apportionment footnote, A1, next to it. Let's see what it has to say:

A1 Funds are apportioned with the understanding that (1) the Department of Homeland Security (DHS) will provide OMB with a spend plan for the amounts appropriated in Sections 90005 and 90006 of the One Big Beautiful Bill Act, P.L. 119-21, detailing the proposed use of funds in an agreed upon format; and (2) DHS will continue to work closely with OMB on any material changes to the spend plan during the period of availability of such funds. [Rationale: OMB requests additional information on programmatic spending for some or all of the apportioned funds.]

Given this footnote, you can get an idea of what's going on-OMB and the agency haven't agreed on how to spend the remaining funds, and OMB wants a spend plan before they allocate that remaining $2 billion in funding. This is fairly common in cases where the funding comes from outside the typical budget process. In this case, the funds came from OBBBA, which was done through a reconciliation bill and wasn't part of the President's budget request.

Also, note the part in brackets: "[Rationale: OMB requests additional information on programmatic spending for some or all of the apportioned funds.]" An A footnote provides a rationale for why the footnote is needed. They're mostly boilerplate, but give you clues as to why OMB thinks this footnote is necessary.

Other Common Types of A Footnotes

These are actual footnotes from recent OMB apportionments.

Adjustments between lines:

Adjustments are permitted between the Medical Assistance Payments category (line 6011) and another category B line where OMB receives written notification 5 business days in advance and where the total of any adjustments does not increase the receiving category by more than 10 percent of the apportioned amount. [Rationale: Footnote specifies the purpose(s) for which the funds are available to be obligated.]

075-0512 /X - Grants to States for Medicaid, Dec. 12, 2025

Notification requirements:

As required by section 111(a) of division B of Public Law 116-93, amounts apportioned on this line are available for obligation after OMB approves a detailed spend plan for such amounts, and 15 days after notifying the Committees on Appropriations of the House of Representatives and the Senate. [Rationale: An agency spend plan or other documentation is necessary to better understand how the agency intends to obligate some or all of the apportioned funds.]

013-0133 /X - Nonrecurring Expenses Fund, Feb. 21, 2025

CISA shall provide the notification and report required by subsections (a) and (b), respectively, of section 2235 of the Homeland Security Act of 2002 (6 U.S.C. 677d) to the EOP at the same time that CISA transmits such notification and report to the applicable congressional committees. [Rationale: OMB requests additional information on programmatic spending for some or all of the apportioned funds.]

070-1911 2022/2028 - Cybersecurity Response and Recovery Fund, Sep. 30, 2025

Conditional release:

Amounts apportioned on this line are available for obligation consistent with the latest agreed-upon spend plan pertaining to such amounts between the agency and the Office of Management and Budget (OMB). Such spend plan submitted by the agency shall include: the allocations of such amounts by program; specific information on current and anticipated grants and contracts utilizing such allocated amounts; and a detailed description of how such spending plan aligns with Administration priorities. Any revisions or additions to such spend plan shall be proposed to OMB in writing no later than five business days before the anticipated obligation of funds based on such revisions or additions. If OMB agrees to such revision or addition, the latest agreed-upon spend plan shall include such revision or addition. In the absence of an agreed-upon spend plan between the agency and OMB, the agency may obligate funds on this line only as necessary for Federal salary and payroll expenses or to make payments otherwise required by law. [Rationale: An agency spend plan or other documentation is necessary to better understand how the agency intends to obligate some or all of the apportioned funds.]

012-3510 /X - Special Supplemental Nutrition Program for Women, Infants, and Children, Dec. 9, 2025

Spending prohibitions:

None of the amounts apportioned are available for obligations of baseload generation or generating plants (whether new or existing) that utilize carbon sequestration systems, as the subsidy rate does not include an assumption of such costs. RUS must consult with OMB on the budgetary treatment of any baseload generation project or project utilizing carbon sequestration systems prior to any such obligations. [Rationale: Footnote specifies the purpose(s) for which the funds are available to be obligated.]

012-1230 2022/2031 - Rural Electrification and Telecommunications Loans Program Account, Sep. 1, 2025

Reporting requirements:

Funds on these lines are apportioned with the understanding that DSCA will provide OMB with a monthly briefing on the status of resource execution. [Rationale: OMB requests additional information on programmatic spending for some or all of the apportioned funds.]

011-8242 /X - Foreign Military Sales Trust Fund, Sep. 30, 2025

Funds in addition to automatic apportionment:

In addition to the amounts apportioned, this account is also receiving funds pursuant to H.R. 5371 as automatically apportioned via OMB Bulletin 26-01. [Rationale: Footnote signifies that this TAFS has received or may receive an automatic apportionment.]

070-0100 /2026 - Operations and Support, Nov. 28, 2025

Presidential policy:

As permissible by law, amounts apportioned shall be spent in a manner consistent with the directives provided in the following: Executive Order 14151, "Ending Radical And Wasteful Government DEI Programs And Preferencing." [Rationale: Footnote specifies the purpose(s) for which the funds are available to be obligated.]

091-0202 2026/2027 - Student Aid Administration, Dec. 19, 2025

Where Footnotes Come From

Footnotes may implement:

- Specific provisions in appropriations law

- Committee report language (non-binding but politically significant)

- Administration policy priorities

- OMB management concerns

Putting it Together

Take this footnote from USDA's Rural Utilities Service as an example:

None of the amounts apportioned are available for obligations of baseload generation or generating plants (whether new or existing) that utilize carbon sequestration systems, as the subsidy rate does not include an assumption of such costs. RUS must consult with OMB on the budgetary treatment of any baseload generation project or project utilizing carbon sequestration systems prior to any such obligations.

Assume that the account has $100 billion in it and the agency obligated exactly $1 for "baseload generation that utilized carbon sequestration systems". If that were to happen, the agency has broken the law and violated the Antideficiency Act. This footnote is an A footnote, has the force of law, and sets the limit for such baseload generation projects at $0. $1 is more than $0-you've exceeded a legal cap. That's an example of how A footnotes can be used to shape and control the execution of appropriation funds.

Reading Footnotes

When you see footnotes, ask:

- Is this a hard legal requirement (from statute) or soft guidance (from report language)?

- Does this limit how funds can be used, or just require notification?

- Who has to approve before the agency can act?

Footnotes can significantly constrain agency flexibility even when dollar amounts are technically apportioned.

The Anti-Deficiency Act: Budget Jail, Revisited

The Anti-Deficiency Act (31 U.S.C. § 1341) makes it illegal to obligate or spend more than Congress appropriated—or more than OMB apportioned.

What Happens When You Violate It

If an agency obligates $30M in Q1 when only $25M was apportioned:

- Immediate reporting to the President and Congress

- Investigation to identify responsible officers

- Administrative discipline (reprimand, suspension, removal)

- Possible criminal referral (fines up to $5,000, imprisonment up to 2 years)

This isn't theoretical. GAO maintains a database of ADA violations, and agencies report new violations regularly. The ADA was designed to prevent agencies from running out of money mid-year. Congress gave OMB the power and responsibility to apportion funds to directly address this issue.

Reapportionments: Living Documents

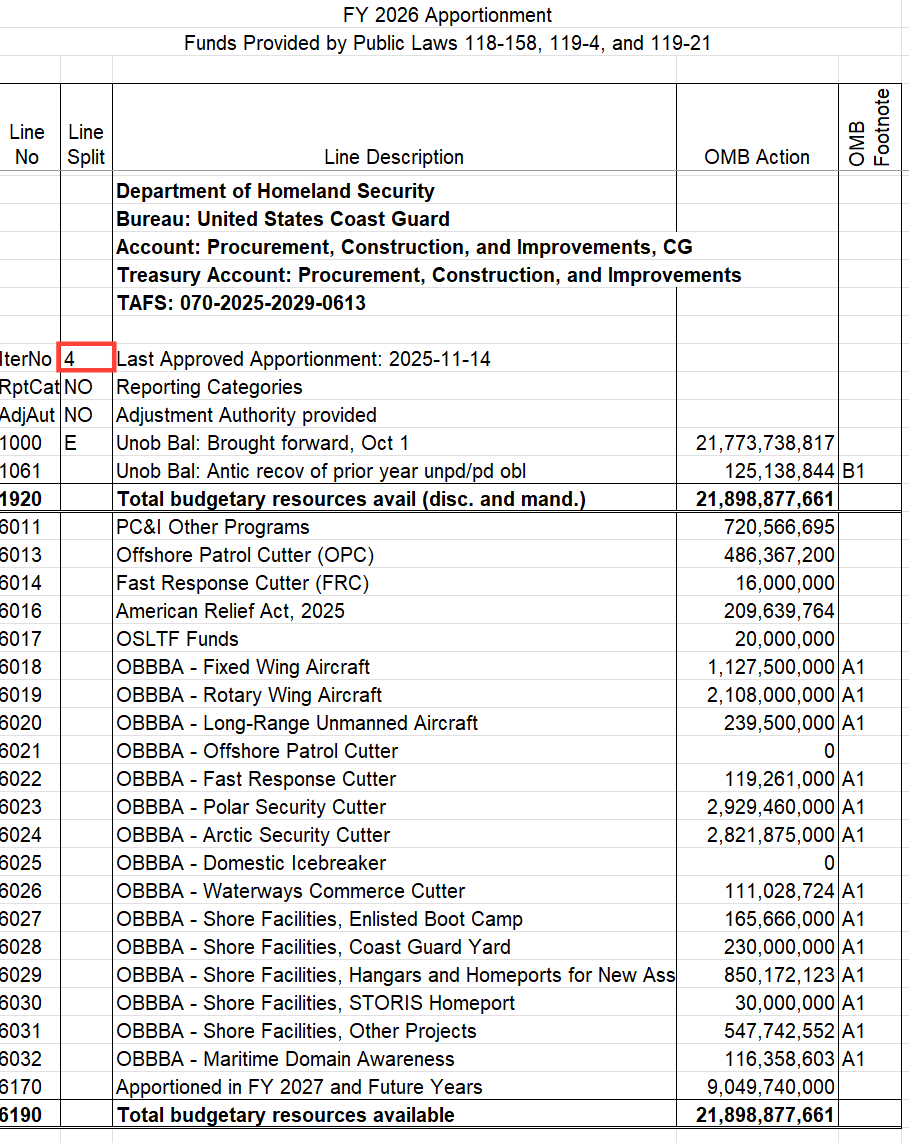

Apportionments change frequently. A single account might have 5, 10, or more versions per fiscal year. Below is the Coast Guard's Procurement, Construction, and Improvements apportionment for the funding provided in the One Big Beautiful Bill Act.

Source: OMB | OpenOMB.org

This is the 4th iteration of the apportionment since the fiscal year started. While the document directly from OMB doesn't show you the changes, the OpenOMB.org version shows a comparison against the most recent apportionment. In each iteration, OMB has apportioned funding that changes the allocations in Category B activities and reduced the amount in the Category C for FY 2027 and future years. This iteration moved $7.2 billion from line 6170 and distributed it to 10 activities.

Why Reapportionments Happen

- Supplemental appropriations: New money requires new apportionment

- Continuing resolutions: Each CR triggers reapportionment

- Rescissions: Canceled funds must be reflected

- Program shifts: Agency requests to adjust Category B amounts

- Policy changes: Administration priorities evolve

- Corrections: Errors in prior versions

What to Track

When analyzing an account over time:

- Version number: Higher = more changes

- Effective date: When each version became active

- What changed: Compare versions to understand the story

Practical Tip

Always verify you have the current version. An October apportionment may be completely superseded by December. Compare the latest version to a previous iteration to get a sense of how the execution is changing over time.

Reading for Slow Spending or Disruption

One practical application: identifying potential slow spending or disruptions. If you're a grantee, you probably don't care about the particular reason you just want to know if the money is moving. If you're a congressional staffer or someone interested in oversight, the reason—including potential impoundments or funds that may be proposed for rescission—is very important.

Red Flags

Large unapportioned balances without explanation

If Congress appropriated $100M and only $60M is apportioned with $40M sitting unapportioned late in the fiscal year, ask why.

Footnotes suggesting policy holds

Language like "funds withheld pending an approved spend plan" or "amounts apportioned shall be spent in a manner consistent with the directives provided" may indicate either prudent stewardship of the public fisc or nefarious actions. It's not unusual or improper for OMB to ask for a spend plan. It does thwart Congressional intent when OMB never approves that plan and stalls the funding.

Timing doesn't match program needs

If it's Q2 and only Q3-Q4 amounts are apportioned for an ongoing program, something's off.

Cross-Reference with SF-133

Compare apportionment to execution:

- Apportionment: What can be spent

- SF-133: What was spent

If both are low, it might be an apportionment constraint. If apportionment is high but execution is low, it's likely an agency execution issue.

We'll cover how to read the SF-133 in our next series.

The Bottom Line

The category system transforms apportionments from simple allocation documents into precise control instruments:

- Category A (time)

- Category B (program)

- Category AB (time and program)

- Category C (future years)

- Footnotes = Specific conditions and restrictions

Understanding these distinctions lets you read apportionments the way budget professionals do.

What's Next

You now understand both the structure and the control mechanisms in apportionments. Next up: the SF-133—the quarterly execution report that shows what agencies actually obligated and outlaid against their apportionment plans. If the apportionment sets the speed limit, the SF-133 is the monthly speedometer.

BlazingStar Analytics is building real-time budget execution tracking that connects appropriations, apportionments, and SF-133 reports. Get early access to our platform, launching Spring 2026.