How to Read an Appropriations Bill, Part 3: Account Text

A single appropriations account can contain $38 billion, six numbered paragraphs, 49 provisos, an "of which" clause, and span multiple pages. How do you read that?

1. Where to start?

2. Structure

3. Account Text

4. General and Administrative Provisions

5. Reports and Explanatory Statements

In Part 2, we covered the structure of an appropriations act—divisions, titles, and the typography that signals what you're looking at. Now we go deeper: into the account text itself.

This is where the money lives. And this is where Congress hides the constraints, permissions, and guardrails that determine what agencies can actually do with that money.

And before we get started, this is a big article: the longest I've ever written. Accounts are the heart and soul of appropriations bills and the most fundamental unit. If you ask an appropriations staffer what they do, they'll likely tell you what accounts they cover. Accounts are where it happens.

The 60-Second Version

| Concept | What It Means |

|---|---|

| Time | When can you spend it? (1-year, multi-year, no-year) |

| Purpose | What can you spend it on? (the account scope + provisos) |

| Amount | How much? (lump sums, line items, floors, ceilings) |

| Provisos | The "provided that" clauses that constrain or expand |

| Of which | Carve-outs within the total—nested allocations |

| Transfer authority | Can you move money to another account? Under what conditions? |

| Report tables | Sometimes Congress makes report language legally binding |

Key insight: Every appropriation answers three questions—time, purpose, amount. Everything else is elaboration on those three.

Click here for a quick explainer.

Part I: The Simple Account

Let's start with something readable. Here's a basic Salaries and Expenses account:

Breaking It Down

The purpose: "For necessary expenses of the Financial Crimes Enforcement Network"—this is the purpose of this appropriation. The purpose usually appears first in an appropriation and begins with the word "for". The agency can only spend this money on activities that fall within this description. Of all of the ways to write an appropriation, "for necessary expenses" is by far the most broad. Also, see the "including, hire of passenger motor vehicles...with or without reimbursement" part? "Including" means these are specific examples of potential necessary expenses, not the only ones.

The amount: $185,193,000 — this is the top-line appropriation.

The time: Look for the availability language. Common patterns:

| Language | Meaning |

|---|---|

| "to remain available until September 30, 2028" | Two-year money. |

| "to remain available until expended" | No-year money. Stays available indefinitely. |

| If it doesn't mention a time, it's one-year money. Expires September 30, 2026. |

This account actually has two different periods of availability.

| Amount | Duration |

|---|---|

| $185,193,000 | One-year money |

| not to exceed $55,000,000 | September 30, 2028 |

We'll cover amount modifiers further later in the post, but not to exceed means any number from $0-$55,000,000. If the agency chose, say, $10 million to be available until 2028, the amount of one-year money would be reduced by $10 million to maintain the total appropriation of $185,193,000.

Key insight: Appropriations are usually written in a Purpose + Amount + Time construction.

- Purpose: "For necessary expenses of the Financial Crimes Enforcement Network"

- Amount: $185,193,000

- Time: silent, so 1-year

The limitation: See that "not to exceed $25,000 for official reception and representation expenses"?

Translation: Congress is saying "you get this money, but you can only spend $25,000 of it on receptions, meetings with stakeholders, and the little cookies they serve at conferences." This is a classic constraint—capping a category of spending that Congress views as potentially wasteful. (FinCEN gets $25K because they do international financial intelligence work—lots of foreign meetings. Other agencies get less.)

Putting it together: I like making diagrams of the funding in an account. Here's an example of what's going on in this one:

Even in a fairly straightforward appropriation, things can get complicated quickly. But the core principles remain-focus on purpose, amount, and time.

Part II: The Complex Account

Now let's look at something gnarlier. Some accounts read like a legal flowchart:

This is harder to parse. Let's diagram it.

The "Of Which" Chain

When you see "of which," Congress is carving out a portion of the total for a specific purpose. These can nest:

Translation: The total is $3 billion, but it's not a blank check. Congress has pre-allocated portions to specific programs, and some of those allocations have their own constraints.

Inheritance: Reading the Tree

Here's a subtle but critical point: carve-outs inherit the attributes of their parent allocation.

The $186M is 2-year money. That means Tax Counseling for the Elderly ($12M), low-income clinics ($28M), and VITA ($46M) are also 2-year money—they're carved from the 2-year pot.

But the Taxpayer Advocate Service ($271.2M) is carved directly from the main appropriation, not from the 2-year proviso. So it's 1-year money.

Remember how I mentioned earlier that if the account doesn't explicitly mention a period of availability, it's one year money? That's an example of inheritance in action. At the top of every appropriations bill there's a statement of appropriations. In this particular bill, it's section 5.

The following sums in this Act are appropriated, out of any money in the Treasury not otherwise appropriated, for the fiscal year ending September 30, 2026.

That statement of appropriations and it's "sums..are appropriated...for the fiscal year ending September 30, 2026" sets the default period of availability for every account in the bill.

If you don't read the tree structure correctly, you'll get the availability wrong.

Floors vs. Ceilings

Watch the language carefully:

| Language | Meaning | Flexibility |

|---|---|---|

| "of which $X shall be for" | Exactly this amount | None—it's a mandate |

| "of which not less than $X" | At least this amount | Can spend more |

| "of which not more than $X" | No more than this amount | Can spend less |

| "of which up to $X may be used" | Optional, capped | Maximum flexibility |

"Not less than" is a floor—Congress is protecting a priority. "Not more than" is a ceiling—Congress is constraining something they're skeptical of.

I wish this was cut and dried, but it isn't. The use of discretion and flexibility with modifiers—and Executive discretion more broadly—is an area of controversy and some subjectivity. For example, Congress doesn't really care if FinCen spends $0 or $25,000 on receptions, they just want to make sure that it's not more than $25,000. Other times Congress will say "not to exceed" and really not mean the $0 part. Similarly, in an "$X shall be for Y" construction, in implementation it usually means as close to that number as is prudent without going over.

Bottom line: Congress clearly has feelings about the use of these particular funds, otherwise the words wouldn't be there.

Numbered Paragraphs: A Cleaner Structure

Some accounts use numbered paragraphs instead of nested prose. Let's look at the

Department of Transportation—Maritime Administration—Operations and Training account. This is easier to read—but the same principles apply:

It's a lot, I know. It gets clearer when you diagram it.

Translation: One account, five different pots of money with three different expiration rules. Congress wants USMMA operations to spend down regularly (2-year), but capital improvements can take years—so they get no-year money.

The numbered format is cleaner than nested "of which" prose, but the logic is identical. Each paragraph is a carve-out with its own availability and purpose.

And note the provisos at the end. They apply to all of the funding in the account.

Part III: Account Archetypes

Not all accounts work the same way. Here are the major archetypes you'll encounter:

Currently Authorized Programs

In the "Schoolhouse Rock" version of legislating, all appropriations would be backed by a current authorization bill that specifies terms and conditions for the program. When that's the case, the appropriations text can be very brief. Here's an example from the VA:

In these two lines, Congress spends $38.7 billion without saying much. The key is this "pursuant to chapter 17 of title 38, United States Code". If you look at that chapter of the Code, you'll find pages and pages of law that deal with who can get that money, how it's allocated, when it's paid and all of the exceptions and special provisions that come with it. This is as pure as it gets for the appropriations-authorization relationship.

Translation: When a program is authorized and the program is well-defined, the appropriations language can be very short.

Key signals:

- "pursuant to [insert code citation]"

- "as authorized by [insert code citation]"

- "carry out the program under [insert code citation]"

Minor Policy Changes

Sometimes the authorization is pretty good, but before the program can be authorized again, the Congress uses an appropriations bill to do a little light surgery on the authorization. Unless explicitly declared in the appropriations act, these changes only last for the fiscal year. Take a look:

Ok. Let me walk you through it. The appropriation is $514 million, for the program in 49 U.S.C. 41731-41742. The money is no-year. This is simple and straightforward. But then you get to the first proviso, something about "the Secretary may consider the relative subsidy requirements". And the second proviso just turns off 49 U.S.C. 41732(b)(3). And the third changes the speed of availability of money under 49 U.S.C. 41742(b). And the last proviso just says that 49 U.S.C. 41731 requirements don't apply. What's going on here? These provisos are changing the application of current law. It's like amending the statute, except that it only lasts for one year and only applies to these funds.

Translation: Congress can modify how existing authorized programs work in an appropriations act.

Key signals:

- "notwithstanding"

- "shall not apply"

- "shall be applied by substituting [X] for [Y]"

Pro tip: If you see "notwithstanding" pay attention. If you see "notwithstanding any other provision of law" pay close attention. This means that there is a policy change coming and what ever follows the notwithstanding is the new policy.

Advance Appropriations

I snuck something past you. The VA, Medical Community Care account is very special. In fact, only a handful of accounts in the government have that construction. Pay close attention to the wording:

Let's start with this observation: fiscal year 2026 started on October 1, 2025 and ends on September 30, 2026. But the text says: "shall become available on October 1, 2026". That's the day after the fiscal year ends!

What you're seeing here is called an advance appropriation. In some accounts, continuity of funding is so important that Congress provides funds a year in advance. In this case, we're in the FY 2026 bill reading the appropriation for FY 2027. And of that amount $2 billion is two-year money.

Key signals:

- "shall become available on"

- "shall be available on"

Translation: In an appropriations act, Congress can provide funding that becomes available in future fiscal years.

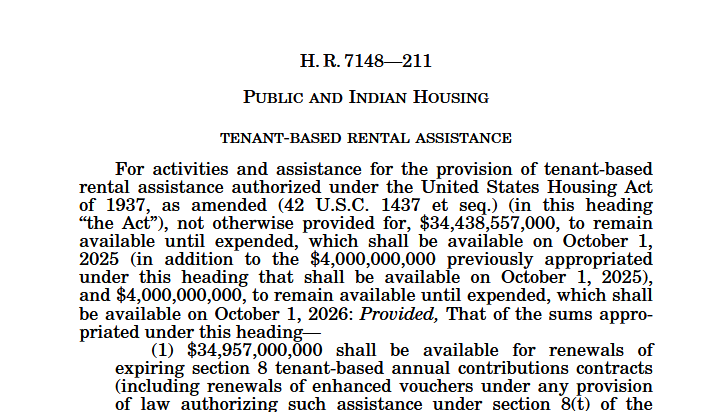

The reason: There are two- advance planning and to avoid service disruption. A few of the programs that receive advance appropriations are Veteran's Affairs Programs, particularly Veterans' Health Programs and HUD's Tenant-Based and Project-Based rental assistance programs. In the VA's case, abruptly running out of funding for Veteran's hospitals wouldn't be a good look. HUD's rental assistance programs run on a calendar year basis and the advance appropriation was intended to bridge the first quarter of the fiscal year. But these accounts are relatively rare and are subject to a Committee-wide cap on aggregate amounts.

Loan Programs

Credit programs don't appropriate the full loan amount—they appropriate the subsidy cost:

Translation: This isn't $64.6 million in loans. This is $64.6 million to cover the cost of making $12.5 billion in loans—the expected defaults, interest rate differentials, and administrative expenses. The actual loan authority is much larger than the appropriation.

Key signals:

- "cost of direct loans" or "cost of guaranteed loans"

- References to the Federal Credit Reform Act (section 502 of the Congressional Budget Act of 1974)

- Loan levels stated separately from appropriated amounts

I'm going to level with you-credit programs are hard. They are some of the most complicated parts of the federal budget. I'm going to cover this someday in a future post. But even for me, credit programs are tough stuff. If you want to nerd out, check out the credit supplement to the President's budget request. Or not. You do you.

Part IV: "For an Additional Amount"

Let's start by looking at this account in the Small Business Administration:

You're like, that's nice, there's $323,118,000 available for SBA salaries and expenses. But wait! You keep reading, and in the administrative provisions for SBA you see:

What It Means

"For an additional amount" signals that Congress is adding money on top of a base appropriation. There's are two principles in appropriations law that make these words a necessity. First, the more specific governs over the general. Second, the more recent governs over the older. When you see appropriations with "for an additional amount", Congress is saying-you can use both pots of money, just make sure you mind the terms and conditions.

You'll see this in two contexts:

In annual appropriations bills:

As in our example above, the base appropriation appears earlier in the bill (or in a prior year's bill still in effect), and Congress is stacking additional funds—often with different terms, availability, or purpose restrictions.

In supplemental appropriations:

Emergency or supplemental bills frequently use this language. The base account exists in the annual bill; the supplemental adds more. Here's an example for FEMA's Disaster Relief Fund from the “Disaster Relief Supplemental Appropriations Act, 2025”:

In a supplemental appropriation like this, the money is just appropriated into the account that exists in a prior appropriations act, and inherits all of the terms and conditions that already exist. Any provisos in the supplemental appropriation apply only to that money.

Note the proviso in pink—you'll see that in nearly every supplemental appropriations act for natural disasters. That's an emergency designation. It means that Congress has decided that these funds are for an emergency and they do not count against the budget caps for this particular fiscal year.

Why It Matters

| Scenario | What to Watch |

|---|---|

| Same bill, different terms | The additional amount may have different availability (no-year vs. one-year) or different purpose constraints |

| Supplemental funding | Often tied to emergencies, disasters, or urgent needs—may have special reporting requirements |

| Stacked provisos | The additional amount may have its own provisos separate from the base account |

Translation: When you see "for an additional amount," you're not looking at the whole picture. Find the base appropriation. Add them together. Then read both sets of provisos—they may differ.

In our SBA example above, we have 2 different appropriations to one account:

| Purpose | Amount | Time |

|---|---|---|

| For necessary expenses... | $323,118,000 | 1-year and 2-year |

| for initiatives... | $106,862,000 | 1-year |

In this case, Congress is appropriating funds to one account with two different purposes, and uses the "for an additional amount" construction to put money on top of the base Salaries and Expenses appropriation for a different purpose. In fact, if you look at the last proviso of Sec. 542, you can see that Congress feels very strongly that these funds can only be used for the specified purposes. They did something extra special here, and that brings us to our next section.

Part V: When Report Language Becomes Law

Remember that SBA administrative provision from the last section? Look at it again: "in the amounts and for the projects specified in the table that appears under the heading 'Administrative Provisions—Small Business Administration' in the explanatory statement..." That phrase just made committee report language legally binding. That's a sophisticated move Congress uses to maintain control.

Normally, committee report language is guidance—agencies should follow it, but it's not legally binding.

But sometimes appropriators make it binding. In the SBA example above, the "for an additional amount" is for community projects, or Congressionally directed spending, or put simply-earmarks. Let's look at it again:

Remember how an appropriation has three elements—time, purpose, and amount? Well, this move says that for purpose and amount, use the data in the table. The time is inherited from Sec. 542, which in turn inherits the period of availability from "Small Business Administration—Salaries and Expenses". Together, this construction made every element in the table an appropriation. Neat, right? Here's a few lines from the table:

| Project Name | Recipient | Recommended ($) |

|---|---|---|

| Set Up Shop: Empowering Entrepreneurs in Underserved Communities |

Anchorage Community Land Trust (ACLT) |

200,000 |

| Athens State University LaunchBox | Athens State University | 205,000 |

| University of North Alabama Center for Innovation |

University of North Alabama |

5,000,000 |

| City of Phoenix Start-Up Commercialization Accelerator |

City of Phoenix | 925,000 |

You can view the full table here.

But this technique doesn't have to be only for earmarks. Consider the HHS—Health Resources and Services Administration-Health Workforce account:

See the highlighted text: "which shall be for the purposes and in the amounts specified in the “Final Bill” column for Health Workforce in the “Departments of Labor, Health and Human Services, Education, and Related Agencies Appropriations Act, 2026” table in the explanatory statement"?

Translation: Congress just gave legal force to that table on page 184 of the explanatory statement. It's not guidance anymore—it's law. If you go to that table, You'll see this:

| Final Bill | |

|---|---|

| National Health Service Corps | 130,000 |

| Health Professions Training | 25,422 |

| Centers of Excellence | 15,000 |

| Health Careers Opportunity Program | 2,310 |

| Faculty Loan Repayment | 55,014 |

| Subtotal, Health Professions Training | 97,746 |

| Primary Care Training and Enhancement | 49,924 |

| Oral Health Training | 43,673 |

| Pediatric Specialty Loan Repayment | 10,000 |

| ⋮ | ⋮ |

| Subtotal, Health Workforce | 1,413,776 |

The amounts are in thousands, but in this table, Congress allocated all $1,413,776,000 of the funds appropriated to the Health Workforce account.

This matters because:

- Report language is more detailed than bill text

- It lets appropriators specify detailed funding amounts without cluttering the statute

- It's still binding on the Executive Branch

How to Spot It

Look for "table" and "explanatory statement" in the account text. We call this concept incorporation by reference.

Part VI: Transfers

Sometimes Congress includes language allowing movement of funds between accounts, like this example from HUD's Lead Hazard Reduction account.

First things first. We've got a (including transfer of funds) parenthetical, so we know to look carefully. And then in (3) we see that up to $2,000,000 in total of the amounts made available under paragraph (2) may be transferred to the heading “Research and Technology”.

Translation: HUD can move money from Lead Hazard Reduction to Research and Technology, but only up to $2,000,000. This is controlled flexibility.

The reason: Congress provided this transfer authority for operational efficiency. The Research and Technology account is within HUD's Policy Development and Research (PD&R) office. PD&R conducts all of HUD's research department-wide. So transferring $2 million to do lead hazard research in PD&R makes sense. That office knows how to run and contract research programs. The alternative would be for the Office of Lead Hazard Control and Healthy Homes to set up their own tiny research operation to administer $2 million in research grants. That doesn't make much sense, so Congress granted HUD the ability to transfer these funds.

The opposite: Remember those SBA earmarks from earlier? Congress included this proviso at the end:

That makes sense, if Congress went through the trouble of putting all of the effort into making the funding decisions that led to that table, they'd want them to stick, right? That's what this provision does, it tells the administration to not get any big ideas about these funds. What the bill says they're for, that's it. There's no other use for them.

The Bigger Picture: Transfers and Reprogramming

This proviso is a small example of a larger concept. Agencies need flexibility to respond to changing circumstances, but Congress wants to maintain control. The result is a system of:

- Transfers: Moving money between accounts

- Reprogramming: Moving money within accounts

Both are governed by complex rules—notification requirements, percentage caps, waiting periods, and committee consultation processes.

We'll cover transfers and reprogramming in depth in Part 3: General and Administrative Provisions, where the act-wide rules live.

Why Should You Care?

"I track grants—do I need to know all this?"

Yes. Whether a grant is competitive or formula changes everything—timing, predictability, and who controls the allocation. The account text tells you which you're dealing with.

"I just need the top-line number."

The top-line is often meaningless without the provisos. $500 million "of which not less than $400 million shall be for [specific thing]" means the discretionary portion is only $100 million.

"Report language isn't legally binding though, right?"

Usually, no. But when Congress incorporates it by reference, it becomes binding. Miss that clause and you'll misread the entire account.

"This seems really detailed for an overview."

This is the overview. The detail is the point. Appropriations text is dense because it's doing a lot of work in a small space.

The Bottom Line

Key takeaways:

- Every appropriation answers three questions: time (when), purpose (what), amount (how much)

- Provisos ("Provided, That") add constraints and conditions

- "Of which" clauses create nested allocations—diagram them

- Inheritance: Carve-outs inherit parent attributes (availability, restrictions)—read the tree

- Floors ("not less than") protect priorities; ceilings ("not more than") constrain

- Loan programs appropriate subsidy costs, not loan amounts

- "For an additional amount" means stacked funding—find the base, read both sets of provisos

- Report tables can become legally binding when incorporated by reference

- Transfers move money between accounts; reprogramming moves it within—both have rules

What's Next

In Part 4: General and Administrative Provisions, we'll zoom out from individual accounts to the provisions that apply across titles, divisions, and the entire act. This is where Congress sets the ground rules—transfer authorities, hiring freezes, policy riders, and the constraints that shape how every dollar gets spent.

That's also where the political fights live. See you there.

BlazingStar Analytics is building real-time budget execution tracking that connects appropriations, apportionments, and SF-133 reports. Get early access to our platform, launching later in 2026.