How to Read an SF-133, Part I: Budgetary Resources (1XXX Lines)

Before you can track what was spent, you need to know what was available.

1. What is an SF-133?

2. How to Read an SF-133, Part I: Budgetary Resources (1XXX Lines)

3. How to Read an SF-133, Part II: Status of Budgetary Resources (2XXX Lines)

4. How to Read an SF-133, Part III: Outlays (3XXX Lines)

In our last post, we introduced the SF-133 as the federal government's budget execution report—the document that shows what agencies actually did with their money. Now it's time to learn how to read one.

We'll start at the top: Section 1XXX, Budgetary Resources. This section answers a simple question: What did the agency have to work with?

The 60-Second Version

| Concept | What It Means |

|---|---|

| 1XXX Lines | Resources available for obligation |

| Line 1910 | Total budgetary resources (the number that matters) |

| 11XX vs 12XX | Discretionary vs. mandatory—same thing, different source |

Key insight: The 1XXX section is all about inputs. Before you can understand what an agency spent, you need to know what they had.

Click here for a quick visual explainer.

SF-133: Form and Structure

Let's actually start at the very top. When you open up the spreadsheet, you'll be greeted with a firehose of data. Take this example from last week:

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

If we were on a Zoom or Teams, I'd share my screen, but this ain't that. This is unwieldy, I admit. I highly recommend that you open this link to the current SF-133 for Cemeterial Expenses (21-1805 /26) and follow along.

The tab we're in is "TAFS Detail". It's the one I use the most for a quick peek at the execution in a particular TAFS. Let's get acquainted:

- Up at the top, highlighted in pink, you have the fiscal year (FY 2026) and the name of the file ("Other Defense--Civil Programs").

- To the right, highlighted in green, is the date the file was last updated (January 2, 2026).

- On the left, highlighted in yellow, is a handy set of filters. For example, I went to the "TAFS" box and typed in "21-1805" and selected "21-1805 /26" for this example.

- Highlighted in blue are the monthly column names Nov-Sep, with the quarter ends marked. There is never a column for October.

The takeaway: A way to think of the SF-133 is like a bank statement, except that instead of separate monthly statements, they're all on one sheet, laid out sequentially. Each column represents what happened through the end of that month. Until that month's reporting is in, OMB fills the month with zeroes.

Let's take a look at what a full year of data looks like:

Source: FY 2025 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

This is the same account, just the year prior. If you look at the top, you see that it says "FY 2025" and on the right "2025-12-03". You can also see that each monthly column has data filled in.

Some observations:

- Lines like 1100 will stay the same across the year, because they reflect an appropriation. If there was a supplemental, you'd see a jump in the month it happened.

- Lines like 1120 are zero until something happens.

- Lines like 1134 revert to zero when a full year appropriations bill passes.

Some real talk before we begin: The SF-133 is an incredibly dense and information rich data source. It can answer a lot of questions, but it can also overwhelm and send you down rabbit holes. There are lines in the 133 that I've been looking at for a decade. There are lines in here that I just discovered writing this blog. I'm not going to cover every line, just ones I think are important or interesting. And not every TAFS will have every line.

Now that we've got acquainted with the form and structure, let's dig into the details.

What Are Budgetary Resources?

Put simply: the total budgetary resources available in an account are all the funds available from all sources available in a given year. It's easy to think that budgetary resources = appropriations. This isn't true in all cases-there are many different sources that can flow into an account-there can be transfers in or out, spending authority from fees collected, borrowing authority, contract authority, unobligated balances from a prior year, and even anticipated fees or transfers.

Unobligated Balances: Last Year's Leftovers

Not all money gets spent in the year it's appropriated. When an agency doesn't obligate everything, the remainder carries forward. That's what the 1000 series captures.

Key Lines

| Line | Description |

|---|---|

| 1000 | Unobligated balance brought forward, Oct 1 |

| 1001 | Discretionary unobligated balance brought forward, Oct 1 |

| 1020 | Adjustment to unobligated balance brought forward (+/-) |

| 1021 | Recoveries of prior year unpaid obligations |

Line 1000 is the big one. This is the unobligated balance from the prior year that's available for obligation without new action by Congress. Think of it as your starting bank balance on October 1.

Line 1001 breaks out the discretionary portion. In "split" accounts (accounts with both discretionary and mandatory funding), this tells you how much of the carryover is discretionary vs. mandatory.

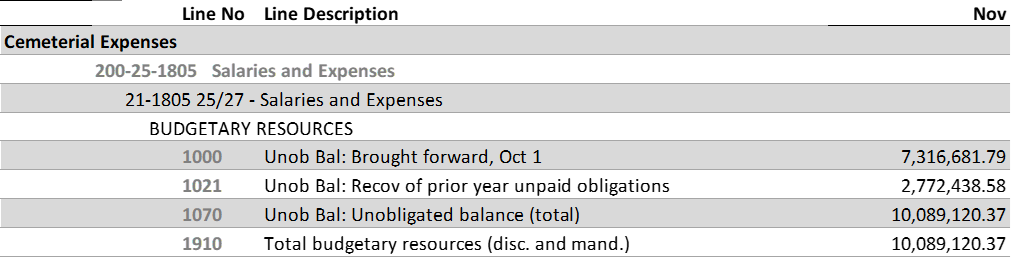

Sometimes unanticipated things happen-a contract runs under or over or a wet construction season means a project didn't get started. That's where lines 1020 and 1021 come in. These lines true up the unobligated balance when reality doesn't match the estimates. This isn't a key component of our example account, but in the companion 3-year Cemeterial Expenses, Salaries and Expenses account (21-1805 25/27), it's a bigger deal. Take a look at the 2026 SF-133 for that account:

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

In this account, all of the budgetary resources available in 2027 are from prior year unobligated balances and recoveries.

Why Carryover Matters

Some accounts routinely carry forward significant balances. This isn't necessarily bad—multi-year construction projects, for example, or multi-year or no-year accounts more generally are designed to spend over several years. But unexpected carryover can signal:

- Execution problems (they couldn't spend the money)

- Program delays (the activity didn't happen as planned)

- Intentional reserves (saving for future needs)

When you see a large amount on line 1000, the question is: why didn't they spend it last year? And the answer is often agency, account and even program specific.

An example, Congress provides HUD with 3-year funding for Homeless Assistance Grants. At the end of year 1, HUD carries over the entire amount into year 2. Should you panic? The answer is probably not. HUD typicially carries over nearly all of the funds from year 1 into year 2 and makes 95+ percent of it's obligations in March-April of the second year. The reason: the funds are awarded competitively and the grant competition starts in year 1, awards are announced in the beginning of year 2, and the obligations follow shortly thereafter. If you see high carryover from year 2 into year 3, it would be cause for concern.

The Continuity Check

Line 1000 should equal the prior year's unobligated balance at year-end. According to OMB A-11:

"The amount on this line should be the same as the end of year amounts of the previous fiscal year: on lines 2201, 2202, 2301, 2302, 2401, 2402, and 2403; or line 2490 of the September 30 SF 133."

If the numbers don't match, something changed between fiscal years—usually an adjustment recorded on line 1020 or somewhere else in the 10XX series.

Transfers: Money Moving Between Accounts

Appropriations don't always stay where Congress put them. Agencies can transfer funds between accounts—when authorized by law. The SF-133 tracks every movement.

Transfer Lines (Discretionary)

| Line | Direction | Description |

|---|---|---|

| 1010 | Out | Unobligated balance transferred to other accounts |

| 1011 | In | Unobligated balance transferred from other accounts |

| 1120 | Out | Appropriations transferred to other accounts |

| 1121 | In | Appropriations transferred from other accounts |

The Two Types of Transfers

Unobligated balance transfers (1010/1011): Prior-year money that moves between accounts. Usually happens under general transfer authority or reorganizations.

Appropriations transfers (1120/1121): New budget authority that moves. This is for transfers authorized by Congress in lieu of appropriations, or where legislation changes the purpose.

Key distinction: Lines 1010/1011 are for old money (balances). Lines 1120/1121 are for new money (appropriations). Don't mix them up.

Mandatory Equivalents

Everything above has a mandatory counterpart:

- Line 1220: Mandatory appropriations transferred out

- Line 1221: Mandatory appropriations transferred in

A word of caution: The SF-133 does not tell you where the money is going to or is coming from. If you're interested in finding out the sources, checking the corresponding apportionment is a great first step. Take a look at Line 1120 on the 2025 Cemeterial Expenses, SF-133. In June, you see -$15,000,000. It's clear they transferred that money out. Where did it go? In the June 3, 2025 apportionment, there's a footnote that gives you the details you need:

B4 Per P.L. 119-4, $15,000,000.00 is transferred from the one-year appropriation (21 2025 1805) to the three-year appropriation (21 2025 2027 1805).

And here you can see the corresponding entry in the 21-1805 25/27 TAFS:

Source: FY 2025 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

The $15 million transfer from the single year account on Line 1120 shows up on Line 1121 in the three year account, both in June. In these transfer transactions, both sides (1120, 1121) should net to zero, because there is no new money involved-just previously appropriated funds.

In this account, the appropriations act allowed for "not to exceed $15,000,000" to be available for 3-years. The agency and OMB effectuated this by first putting all of the $118,780,450 into the single-year TAFS, then transferring out the $15 million later in the year. You'll see this transfer pattern in appropriations with split periods of availability.

Discretionary vs. Mandatory Appropriations: Same Structure, Different Source

Here's something that might confuse people: the SF-133 has parallel line structures for discretionary and mandatory appropriations. Lines 11XX are discretionary; lines 12XX are mandatory. But they mean the same thing—just from different sources of budget authority.

| Discretionary (11XX) | Mandatory (12XX) | What It Represents |

|---|---|---|

| 1100 | 1200 | Appropriation |

| 1101 | 1201 | Appropriation (special or trust fund) |

| 1102 | 1202 | Appropriation (previously unavailable) |

| 1103 | 1203 | Appropriation (previously unavailable, special or trust) |

| 1106 | 1206 | Reappropriation |

| 1120 | 1220 | Appropriations transferred to other accounts (-) |

| 1121 | 1221 | Appropriations transferred from other accounts |

| 1130 | 1230 | Appropriations permanently reduced (-) |

| 1132 | 1232 | Appropriations temporarily reduced (-) |

| 1134 | 1234 | Appropriations precluded from obligation (-) |

| 1135 | 1235 | Appropriations precluded from obligation (special or trust) (-) |

| 1140 | 1240 | Capital transfers to general fund (-) |

Why it matters: When you're analyzing an account, don't get confused by the line numbers. If you see amounts on both 1100 and 1200, the agency has both discretionary and mandatory appropriations in the same account. That's normal for some programs.

The takeaway: 11XX and 12XX are mirror images. Learn one, and you've learned both.

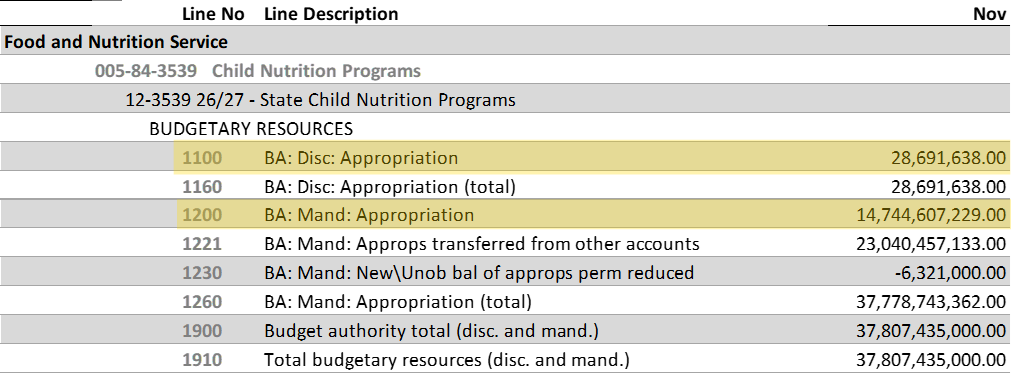

Let's take a look at an account that has both discretionary and mandatory funding sources. This is the SF-133 for USDA's State Child Nutrition Programs Account. We looked at the apportionment for this account in our apportionment series.

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Department of Agriculture

Line 1100 shows a small discretionary appropriation of $28.7 million and line 1200 shows a mandatory appropriation of $14.7 billion. Interestingly, the majority of resources in this account are actually transfers from other accounts! But the structure remains the same-discretionary and mandatory sources are broken out separately in the budgetary resources section and they all feed into the total on line 1910.

Continuing Resolutions: The "Precluded from Obligation" Lines

Here's a line that matters during every CR: Line 1134 (discretionary) and Line 1234 (mandatory).

When an agency is operating under a continuing resolution, they typically get authority at the prior year's rate—but they can only use a portion of it until the CR ends or a full-year appropriation passes. The amount they can't use yet shows up as a negative on line 1134 or 1135. This is identical to how it's handled in the apportionment.

Example: How CRs Appear on the SF-133

Let's use last year's Cemeterial Expenses, Salaries and Expenses Account as an example.

Source: FY 2025 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

FY 2025 had several continuing resolutions (CRs):

- through December 20, 2024

- through March 14, 2025

- through September 30, 2025

On an SF-133, you can see the changes in the 1134 line on this CR. These track the duration of the CR and the OMB calculated prorata amount. For this account:

| Line | Description | December CR | March CR |

|---|---|---|---|

| 1100 | Appropriation | $99,880,000 | $99,880,000 |

| 1134 | Appropriations precluded from obligation | -$77,716,628 | -$54,734,240 |

| 1910 | Total Budgetary Resources | $22,163,372 | $45,145,760 |

Why it matters: During a CR, don't be fooled by the appropriation line. The real amount available is after the 1134 reduction, shown on line 1910.

Spending Authority from Offsetting Collections: Fee-Funded Programs

Not all budgetary resources come from appropriations. Some programs are funded by fees, reimbursements, or other collections. The SF-133 captures these on the 1700 series (discretionary) and 1800 series (mandatory).

Key Lines

| Discretionary | Mandatory | Description |

|---|---|---|

| 1700 | 1800 | Collected (cash received) |

| 1701 | 1801 | Change in uncollected payments, Federal sources |

| 1710 | 1810 | Spending authority transferred to other accounts (-) |

| 1711 | 1811 | Spending authority transferred from other accounts |

| 1740 | 1840 | Anticipated collections |

| 1750 | 1850 | Spending authority, total |

How It Works

When Congress authorizes an agency to spend the fees it collects, that creates "spending authority from offsetting collections." The agency doesn't wait for an appropriation—they spend what they earn.

Line 1700/1800 shows actual cash collected during the year. This includes:

- User fees

- Loan repayments

- Sales of goods or services

Line 1740/1840 shows anticipated collections—money the agency expects to collect but hasn't yet. This is important for budgeting purposes, but it's not real money until it shows up on 1700/1800.

Common Examples

- Passport fees → State Department

- Park entrance fees → National Park Service

- Patent and Trademark fees → U.S. Patent and Trademark Office

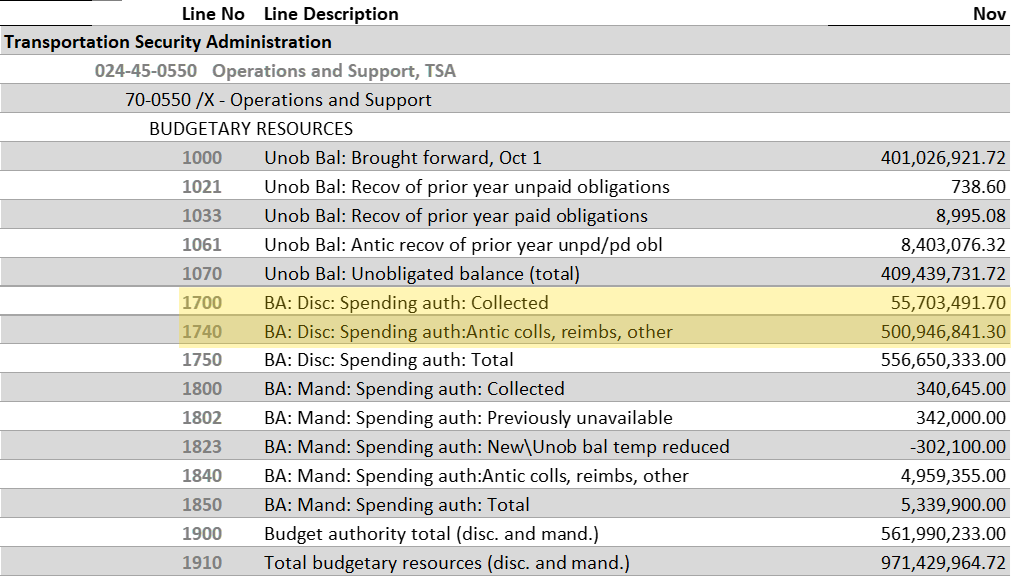

Have you ever wondered what happens to your money when you pay for TSA PreCheck? No? Hasn't crossed your mind? Well, let's take a look. Here's the SF-133:

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Department of Homeland Security

Note that there's no line 1100 or 1200-that means that this account recieves no appropriation. How does it get money? Well, it has a good amount of carryover on line 1000, but take a closer look at lines 1700 and 1740. As fees are collected into this account, say you get or renew your PreCheck, it goes into line 1700, those are actual deposits. Line 1740 is the estimate of what's going to happen over the course of the year. In September, all of the money will be in line 1700 and there will be $0 in line 1740. A good estimate model keeps line 1750 constant throughout the year.

Why It Matters

Fee-funded programs behave differently than appropriated programs:

- Revenue-dependent: If collections fall short, they may not have enough to spend

- Self-sustaining: They don't compete for appropriations (in theory)

- Volatile: Collections can swing based on demand

When analyzing a fee-funded account, watch the relationship between 1740 (anticipated) and 1700 (actual). If actual consistently falls short of anticipated, the agency is chronically overestimating their revenue.

The Math: Internal Consistency

All of this sets us up for next week. The SF-133 is a balanced document. The numbers at the top must equal the numbers at the bottom. Here's how it works:

The Core Equation

Line 1910 (Total budgetary resources) = Line 2500 (Total budgetary resources)

Wait—those are the same thing? Yes. Line 1910 is at the bottom of Section 1XXX. Line 2500 is at the bottom of Section 2XXX. They must be equal.

This is the fundamental integrity check of the SF-133: everything that came in (Section 1) must be accounted for in the status check (Section 2).

How 1910 Is Calculated

Line 1910 equals the sum of:

- All appropriations (1100 series and 1200 series)

- All borrowing authority (1300 series)

- All contract authority (1500 series)

- All spending authority from offsetting collections (1700 series and 1800 series)

- Unobligated balances brought forward (1000 series)

- All adjustments (transfers, reductions, recoveries)

If you're validating an SF-133, this is your first check: does 1910 = 2500? If not, something is wrong.

The Bottom Line

Section 1XXX answers: What did the agency have to work with?

Key takeaways:

- Lines 11XX (discretionary) and 12XX (mandatory) are parallel structures—learn one, know both

- Line 1910 = Total budgetary resources (the number that matters)

- Line 1134/1234 = Amount precluded during a CR (subtract this to see real availability)

- Lines 1010/1011 = Balance transfers; Lines 1120/1121 = Appropriation transfers

- Line 1021 = Recoveries of prior year obligations (deobs)

- Line 1910 must equal Line 2500 (internal consistency check)

What's Next

Now that you know what resources an agency had, the next question is: What did they do with it?

In Part II, we'll cover Section 2XXX: Status of Budgetary Resources. This is where you see obligations, unobligated balances, and the all-important question: did they spend what OMB allowed?

BlazingStar Analytics is building real-time budget execution tracking that connects appropriations, apportionments, and SF-133 reports. Get early access to our platform, launching Spring 2026.