How to Read an SF-133, Part II: Status of Budgetary Resources (2XXX Lines)

Congress provided $100 million. What did the agency do with it?

1. What is an SF-133?

2. How to Read an SF-133, Part I: Budgetary Resources (1XXX Lines)

3. How to Read an SF-133, Part II: Status of Budgetary Resources (2XXX Lines)

4. How to Read an SF-133, Part III: Outlays (3XXX Lines)

In Part I, we covered the 1XXX lines—what resources an agency had to work with. Now comes the interesting part: Section 2XXX, Status of Budgetary Resources. This is where you find out what the agency actually did with the money, or what they obligated.

An obligation is a binding commitment to provide money—a signed contract, a purchase order, a grant award. It's not cash out the door yet, but it's a legal promise that the money is spoken for. In the picture above, you're actually seeing an obligation as it happens. When Secretary Edison signed awards to construct naval vessels, the government incurred an obligation. The money hasn't left the Treasury yet, but signing a contract or an award represents the government's promise to pay.

The 60-Second Version

Key lines in the SF-133: Status of Budgetary Resources section

| Line | What It Shows |

|---|---|

| 2001-2003 | Direct obligations by apportionment category |

| 2101-2103 | Reimbursable obligations by apportionment category |

| 2190 | Total new obligations and upward adjustments |

| 2201-2203 | Apportioned balances (available, future, anticipated) |

| 2301-2303 | Exempt from apportionment balances |

| 2401-2403 | Unapportioned balances (deferred, withheld, other) |

| 2490 | Unobligated balance, end of year |

| 2500 | Total budgetary resources (must equal line 1910) |

Key insight: Section 2XXX is the accountability section. It shows how every dollar of resources was either obligated or left unobligated—and if unobligated, why.

Check out our quick visual explainer.

The Balance That Must Balance

Here's the fundamental equation of the SF-133:

Line 1910 (Total budgetary resources) = Line 2500 (Total budgetary resources)

Section 1 told you what came in. Section 2 tells you where it went. The two must match. If they don't, something is wrong with the data.

Line 2500 is calculated as:

Line 2500 = Line 2190 (Obligations) + Line 2490 (Unobligated balance, end of year)

Or in plain English:

Total resources = What you obligated + What you didn't obligate

This is the core integrity check. Everything the agency had must be accounted for as either obligated or still sitting as a balance.

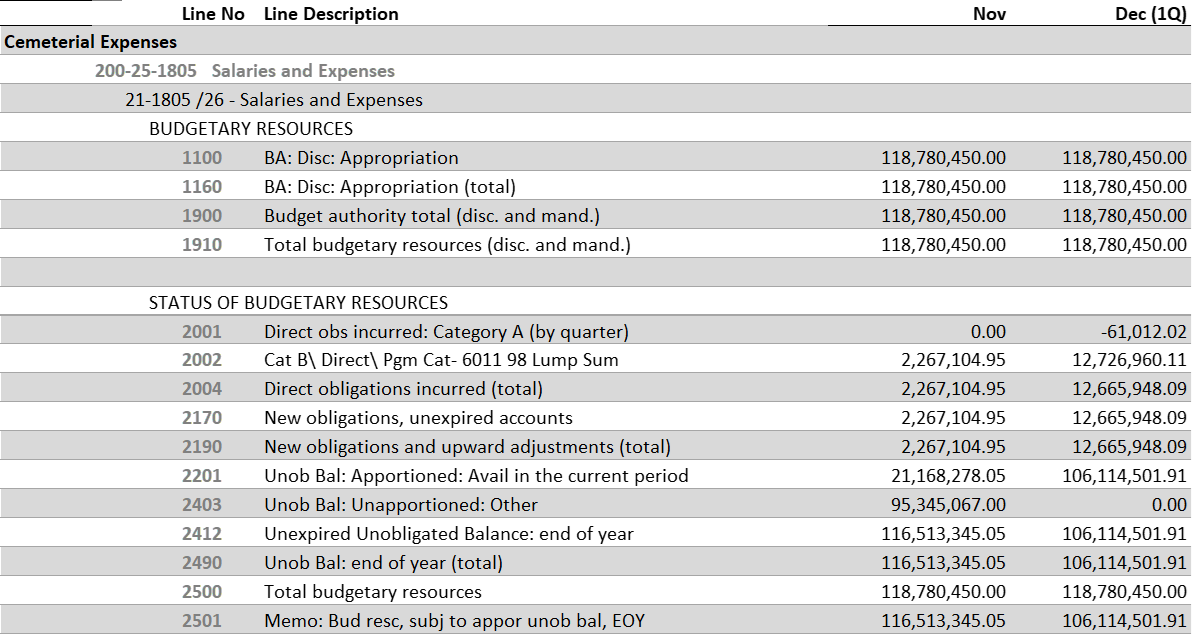

Let's take a look at the Cemeterial Expenses account, or TAFS, shown below.

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

Here are the amounts from the Dec(1Q) column:

| +/-/= | Line | Description | Amount |

|---|---|---|---|

| 1910 | Total budgetary resources (disc. and mand.) | $118,780,450.00 | |

| 2190 | New obligations and upward adjustments (total) | $12,665,948.09 | |

| + | 2490 | Unob Bal: end of year (total) | $106,114,501.91 |

| = | 2500 | Total budgetary resources (disc. and mand.) | $118,780,450.00 |

The formula holds up. Line 1910 = Line 2500. Line 2500 = (Line 2190 + Line 2490).

Putting this together, you now can be the coolest person at barbecues and cocktail parties by saying things like:

- Cemeterial Expenses, Salaries and Expenses (21-1805 /26) had $118.8 million in budgetary resources at the end of December.

- Through that period, the TAFS had obligated $12.7 million, up from $2.3 million at the end of November.

- The TAFS has $106.1 million in resources left to obligate before the end of FY 2026.

If you wanted to really charm folks and wow them, you could even say:

- The TAFS had obligated 10.66 percent of available budgetary resources at the end of Q1 FY26.

And then you'll laugh and look dashing. You'll definitely leave with more friends, and you'll likely leave taller and wealthier too. But this example captures what the Status of Budgetary Resources is all about. From the apportionment, you know that funding was made available to the agency. The Budgetary Resources section shows how much money exists. The Status of Budgetary Resources section shows the agency is putting that money to use.

- The TAFS: The Universal Identifier for Federal Spending

- Appropriations, Obligations, and Outlays: The Three Stages of Federal Spending

Obligations: What They Committed to Spend

The top of Section 2XXX shows obligations—the binding commitments an agency made to provide money. This is where the SF-133 connects back to the apportionment.

The Category A/B Connection

Remember from our apportionment series that OMB apportions funds using categories:

| SF-132 Line | Apportionment Category | SF-133 Line | Obligations Against That Category |

|---|---|---|---|

| 6001-6004 | Category A (by quarter) | 2001 | Direct obligations, Category A |

| 6011-6159 | Category B (by program/project) | 2002 | Direct obligations, Category B |

| — | Exempt from apportionment | 2003 | Direct obligations, exempt |

Why this matters: The SF-133 tells you whether the agency obligated against their Category A (time-based) or Category B (program-based) apportionments. You can compare:

- SF-132 line 6001 (Q1 apportioned amount) → SF-133 line 2001 (Q1 obligations)

- SF-132 line 6011 (Program X apportioned) → SF-133 line 2002 (Program X obligations)

If obligations on line 2001 exceed what was apportioned for that quarter on the SF-132, the agency may have a problem.

And we see that in the Cemeterial Expenses, Salaries and Expenses example. In the SF-133 for Cemeterial Expenses above, line 2002's description is: "Cat B\ Direct\ Pgm Cat- 6011 98 Lump Sum". And if you were to go take a look at the apportionment, you'd see that Line 6011 is: "Lump Sum". These all connect. But I picked Cemeterial Expenses not just because of the important work that it does, but also because of how straightforward the account is. One line called "Lump Sum" is as basic as you can get. Let's take a look at some more complex examples.

Category A: Apportionment by Quarter

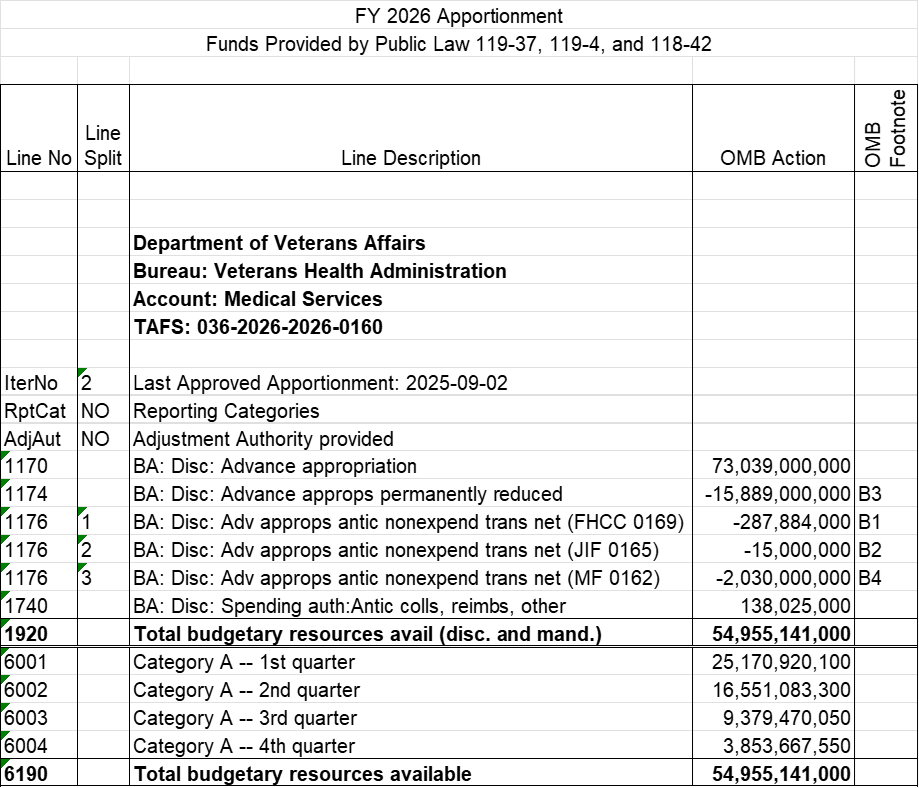

Let's take a look at the most recent apportionment for VA's Medical Services account (36-0160 /26). This is from December 9, 2025:

Source: OMB | OpenOMB.org

The apportionment makes funds available on a quarterly basis in lines 6001-6004:

| Line | Description | Amount |

|---|---|---|

| 6001 | Category A -- 1st quarter | 25,170,920,100 |

| 6002 | Category A -- 2nd quarter | 16,551,083,300 |

| 6003 | Category A -- 3rd quarter | 9,379,470,050 |

| 6004 | Category A -- 4th quarter | 3,853,667,550 |

| 6190 | Total budgetary resources available | 54,955,141,000 |

In reality, the apportioned funds are available in that quarter and each quarter that follows. The availability of funds looks more like this:

| Q1 | Q2 | Q3 | Q4 | |

|---|---|---|---|---|

| 6001 | 25,170,920,100 | 25,170,920,100 | 25,170,920,100 | 25,170,920,100 |

| 6002 | 16,551,083,300 | 16,551,083,300 | 16,551,083,300 | |

| 6003 | 9,379,470,050 | 9,379,470,050 | ||

| 6004 | 3,853,667,550 | |||

| Available | 25,170,920,100 | 41,722,003,400 | 51,101,473,450 | 54,955,141,000 |

| Not Yet | 29,784,220,900 | 13,233,137,600 | 3,853,667,550 | 0 |

| Total | 54,955,141,000 | 54,955,141,000 | 54,955,141,000 | 54,955,141,000 |

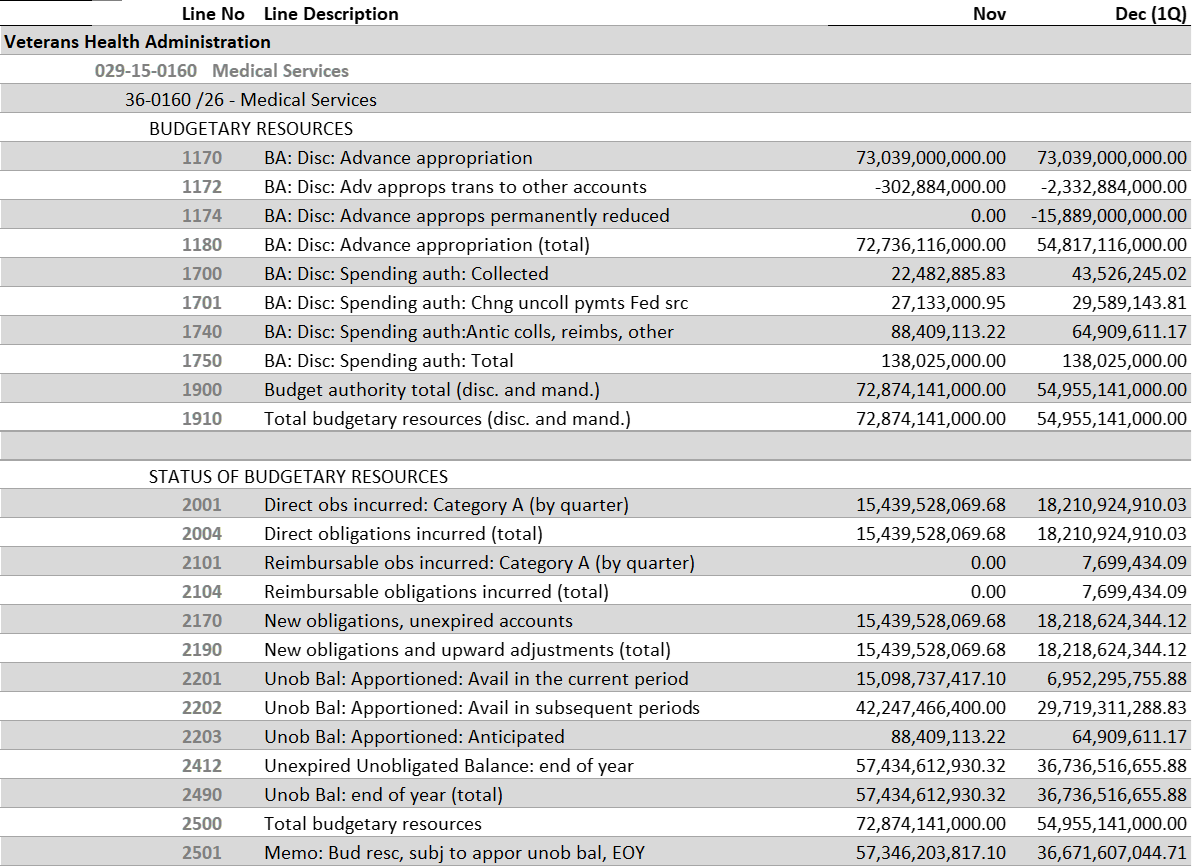

Now take a look at the SF-133:

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Department of Veterans Affairs

Line 2001 shows that this Medical Services TAFS has obligated $18.2 billion against the $25.2 billion available in this quarter. There's another $30 billion available in future periods, shown in line 2202. As the year progresses, you'll see the shift from line 2202 to 2201 to reflect the amounts made available in the quarterly apportionments. Line 2001 accumulates through the year—as each quarter unlocks its apportionment on lines 6001-6004, obligations against those amounts all roll into line 2001.

Category B: Apportionment by Activity

Here's something important: Category B obligations aren't just lumped together. The SF-133 breaks them out by the same project/program codes used on the SF-132.

If the SF-132 apportioned:

- $50M to Capital Improvements (6011)

- $30M to IT Modernization (6012)

- $20M to Training (6013)

Then the SF-133 will show separate Category B detail lines under 2002:

- Capital Improvements: obligations against that $50M

- IT Modernization: obligations against that $30M

- Training: obligations against that $20M

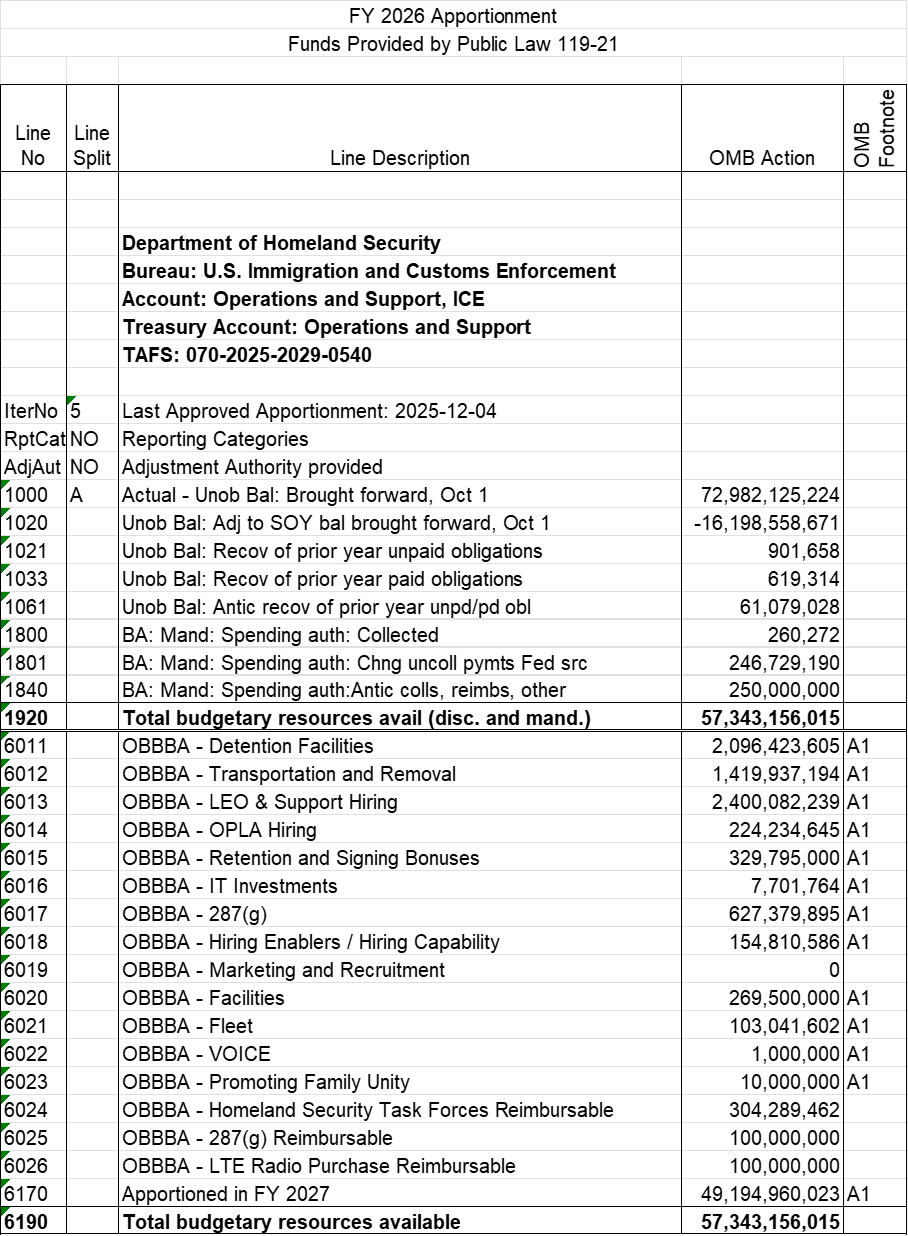

This is how you check whether an agency spent on the right things—not just the right amount, but for the right purposes. Let's analyze a real life example. This is the apportionment for DHS' Immigration and Customs Enforcement, Operations and Support Account, 2025-2029 funding. It's multi-year money provided in last year's reconciliation bill.

Source: OMB | OpenOMB.org

We need to deal with an elephant in the room first. Take a look at line 1020 on the apportionment. -$16.2 billion. That's a lot of money. Line 1020 is "Unob Bal: Adj to SOY bal brought forward, Oct 1". If you're me, that line description might make sense, but if you're you, maybe not so much. Let's go to Appendix F of Circular A-11. Here's the description for line 1020:

Changes to unobligated balances that occurred in a prior fiscal year and that were not recorded in the unobligated balance as of October 1 of the current fiscal year. These may be identified by the financial statement auditors, agency personnel, or others.

Put simply, after the fiscal year closed, as part of the year-end closeout work, someone discovered that there was $16.2 billion less in the account than they initially reported on the last SF-133. This means they needed to adjust the balance at the start of year (SOY). When you look at the SF-133 for the month of December in FY 2026 (spoiler, it's right below), you're not going to see that -$16.2 billion recorded yet. When the January SF-133 is published next month, I expect this adjustment will appear. That SF-133 data should be available in February.

With that caveat out of the way, it shouldn't deter us from digging into the category B examples in this apportionment and SF-133.

Lines 6011 - 6026 on the apportionment apportion funds by program (category B). In these lines, funds are apportioned in specific amounts for specific purposes like:

- Detention Facilities (6011)

- Transportation and Removal (6012)

- LEO & Support Hiring (6013)

- OPLA Hiring (6014)

Line 6170 reserves a portion of the funds for a future fiscal year (category C).

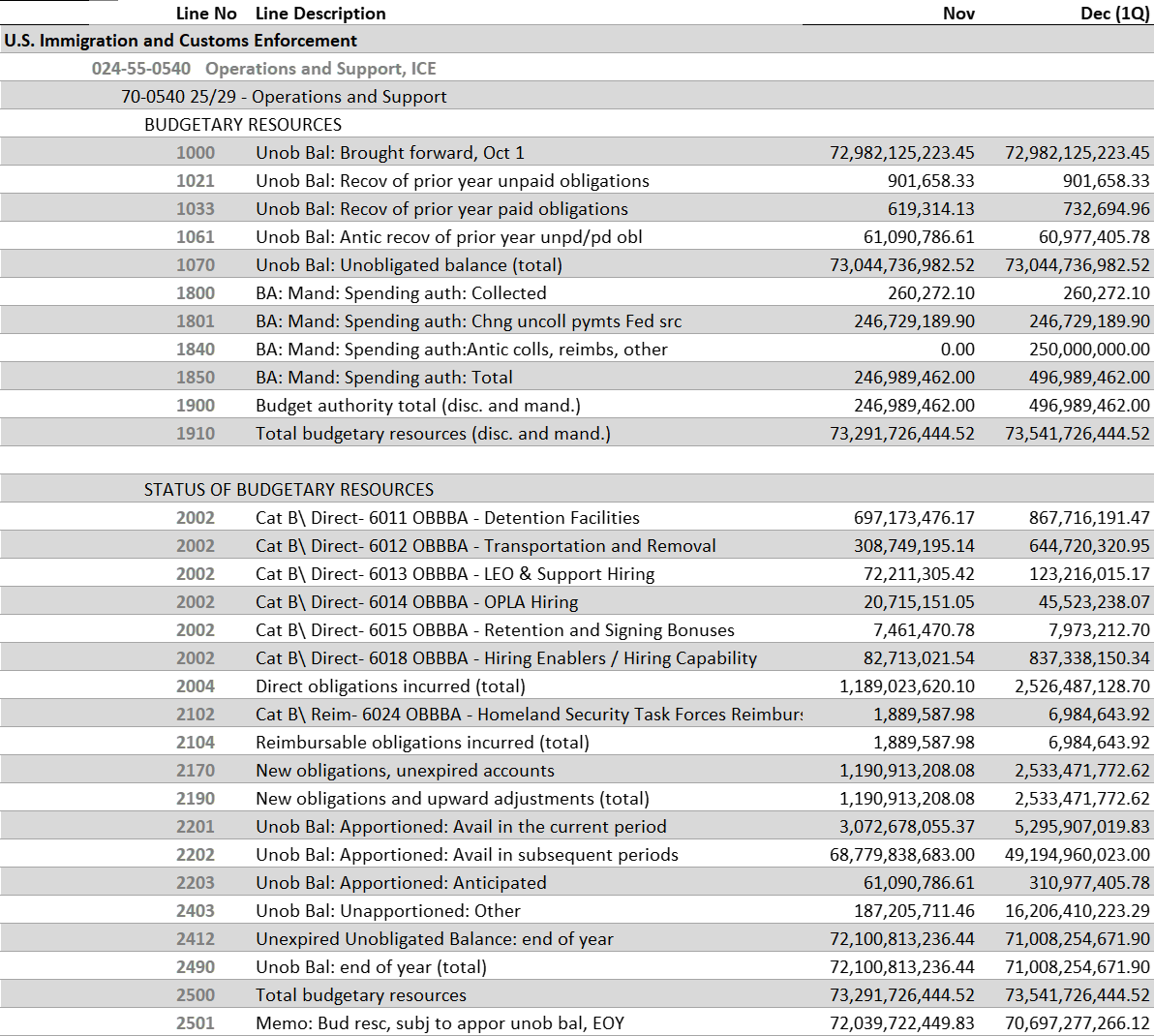

Again, the apportionment sets the speed limit. If you want to know how fast the agency is obligating these funds, you need to look at the SF-133. The most recent SF-133 (through 12/31/2025) follows:

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Department of Homeland Security

Focus on the 2002 lines. Look at the line descriptions; they should seem familiar:

| Line | Dec (1Q) | |

|---|---|---|

| 2002 | Cat B\ Direct- 6011 OBBBA - Detention Facilities | 867,716,191.47 |

| 2002 | Cat B\ Direct- 6012 OBBBA - Transportation and Removal | 644,720,320.95 |

| 2002 | Cat B\ Direct- 6013 OBBBA - LEO & Support Hiring | 123,216,015.17 |

| 2002 | Cat B\ Direct- 6014 OBBBA - OPLA Hiring | 45,523,238.07 |

| 2002 | Cat B\ Direct- 6015 OBBBA - Retention and Signing Bonuses | 7,973,212.70 |

| 2002 | Cat B\ Direct- 6018 OBBBA - Hiring Enablers / Hiring Capability | 837,338,150.34 |

| 2004 | Direct obligations incurred (total) | 2,526,487,128.70 |

I hope you're having a small "Aha!" moment right now. Line 2002 tracks obligations by category B apportionment. You can see that through the end of quarter 1, DHS obligated $867,716,191.47 on detention facilities against an apportioned amount of $2.1 billion. Using these two documents together, you can get a fuller picture of how the agency is executing the funds. The 2002 lines sum to $2.5 billion, shown on line 2004: Direct obligations incurred (total).

Notice line 2202 on the SF-133: $49,194,960,023.00. That's the amount that was apportioned in FY 2027 on line 6170 of the apportionment.

In reality, you'd want a table like this:

| SF-132 Line | Program | Apportioned | Obligated (SF-133) | Rate |

|---|---|---|---|---|

| 6011 | Detention Facilities | $2,096M | $868M | 41% |

| 6012 | Transportation & Removal | $1,420M | $645M | 45% |

| 6013 | LEO & Support Hiring | $2,400M | $123M | 5% |

| 6014 | OPLA Hiring | $224M | $46M | 20% |

| 6015 | Retention/Signing Bonuses | $330M | $8M | 2% |

| 6016 | IT Investments | $8M | $0 | 0% |

| 6017 | 287(g) | $627M | $0 | 0% |

| 6018 | Hiring Enablers | $155M | $837M | ??? |

| 6019 | Marketing and Recruitment | $0 | $0 | — |

| 6020 | Facilities | $270M | $0 | 0% |

| 6021 | Fleet | $103M | $0 | 0% |

| 6022 | VOICE | $1M | $0 | 0% |

| 6023 | Promoting Family Unity | $10M | $0 | 0% |

| 6024 | HS Task Forces (Reimb) | $304M | $7M | 2% |

| 6025 | 287(g) Reimbursable | $100M | $0 | 0% |

| 6026 | LTE Radio Purchase (Reimb) | $100M | $0 | 0% |

| 6170 | Apportioned in FY 2027 | $49,195M | — | — |

| Total | $57,343M | $2,533M | 4.4% |

This table doesn't exist yet, but we're working on creating tools like this when we release our BlazingStar Analytics platform later this spring. It's exercises like this that led me to build the product.

Notice that DHS has executed 41-45 percent of the apportioned amounts for the Detention Facilities and Transportation & Removal activities. The hiring lines and the capital lines are executing slower.

Direct vs. Reimbursable

| Type | Lines | What It Means |

|---|---|---|

| Direct | 2001-2003 | Obligations not financed from reimbursements |

| Reimbursable | 2101-2103 | Obligations financed by payments from other agencies |

Direct obligations (lines 2001-2003) are the main event. This is the agency committing spend its appropriated funds.

Reimbursable obligations (lines 2101-2103) are when one agency does work for another and gets paid for it. Think of it as federal government freelancing—an agency provides goods or services to another entity and charges them for it.

If you look at the example above, you'll note that line 6024, Homeland Security Task Forces is a reimbursable line, and that about $7M has been obligated. At some point in the year, another TAFS will transfer funds into this TAFS to liquidate that reimbursement debt, and it will be recorded in the 18XX lines in the Budgetary Resources section of this TAFS.

And another thing to keep in mind, apportionments can and do change across the course of a fiscal year. For example, the ICE, Operations and Support apportionment we looked at is the 5th version for the year. You need to read the SF-133 against the operative apportionment for that time period.

The Red Flag Zone: When Obligations Exceed Apportionments

According to OMB A-11 Appendix F:

"If, on the September 30 report, a negative amount is reported on [line 2403], the amount must be offset by remaining balances. For accounts that are apportioned, the offset must be against apportioned funds reported on line 2201 or an apparent violation of the Antideficiency Act (31 U.S.C. 1341, 1342, or 1517) will have occurred."

Translation: If an agency obligates more than their resources allow, they've potentially broken the law.

- The Constitutional and Legal Framework: Laws That Control Federal Spending

What to Watch For

| Signal | What It Might Mean |

|---|---|

| Line 2001 > SF-132 line 6001 (cumulative) | Obligated faster than quarterly pace allowed |

| Line 2002 detail > corresponding SF-132 6XXX detail | Over-obligated a specific program |

| Negative line 2403 | Resources fell short of expectations |

The Antideficiency Act makes it illegal to obligate more than Congress appropriated or more than OMB apportioned. The SF-133 is the document that proves whether an agency stayed within bounds.

Ok. You're probably thinking, I just saw this didn't I? Let's take a closer look at DHS, Immigration and Customs Enforcement, Operations and Support, line 6018:

| SF-132 Line | Program | Apportioned (12/31) | Line 2002 (Nov) | Line 2002 (Dec) |

|---|---|---|---|---|

| 6018 | Hiring Enablers | $155M | $83M | $837M |

Clearly $837M is more than $155M. If ICE truly obligated $837M against a $155M apportionment, that would be a clear Antideficiency Act violation.

But, as with all things Federal data related, there could be another explanation. $837M is almost exactly 10x $83M. It could literally be that someone fat fingered an entry and put an extra zero where one doesn't belong. There could be a missing apportionment. Either way, this is a great example of why it's important to look at the 133 alongside the apportionment.

Unobligated Balances: The Money They Didn't Spend

Not everything gets obligated. The 2200, 2300, and 2400 line series show what's left over—and importantly, why it's left over.

Apportioned Balances (Lines 2201-2203)

| Line | Description |

|---|---|

| 2201 | Available in the current period |

| 2202 | Available in subsequent periods |

| 2203 | Anticipated (+ or -) |

These are balances that could be obligated—the agency has permission from OMB, they just haven't done it yet.

Line 2201 is particularly interesting: this is money that was apportioned for the current period and hasn't been obligated. At the end of Q1, if line 2201 shows a large balance, the agency is behind on execution.

Line 2202 shows money apportioned for future quarters (Category A) or future years (Category C). This isn't available yet—it's in the queue.

The VA, Medical Services and ICE, Operations and Support TAFS demonstrated this. You saw the category A amounts for future quarters show up in 2202 in the VA, Medical Services example. ICE, Operations and support put the funds apportioned in 2027 in the same line—2202.

Line 2203 An intrepid observer might have noticed that the SF-133 for the VA, Medical Services account had $65 million in line 2203. That corresponds to anticipated collections shown on line 1740 that have not actually materialized yet. As those collections are received, they'll move to line 2201.

Exempt Balances (Lines 2301-2303)

Some accounts don't require apportionment—they're "exempt." These are pretty rare. Trust funds, certain fee-funded programs, and some others operate outside the normal apportionment process. Lines 2301-2303 track their unobligated balances.

Unapportioned Balances (Lines 2401-2403)

Here's where it gets politically interesting:

| Line | Description | Source |

|---|---|---|

| 2401 | Deferred | SF-132 line 6181 |

| 2402 | Withheld pending rescission | SF-132 line 6180 |

| 2403 | Other | Everything else |

Line 2401 (Deferred) and Line 2402 (Withheld pending rescission) are where you see executive branch constraints. If the President has proposed rescinding funds or is deferring spending, these balances will appear here.

During impoundment controversies—like the ones we've seen in recent years—these lines tell the story. Significant amounts on lines 2401 or 2402 indicate that funds Congress appropriated are being held back by the executive branch. If you ever see an amount in these lines, it's immediately interesting. There's either a proposal to defer or rescind from the Executive Branch to Congress or some sort of inter-branch power play brewing.

Line 2403 (Other) is a catch-all for unapportioned balances that aren't deferred or withheld. This includes excess resources above what's been apportioned, and the unapportioned balance of revolving funds.

Reading the Execution Story

Let's put it together, with some hypotheticals to illustrate the concepts. Here's what a healthy account looks like at the end of Q3:

| Line | Description | Amount | % of Total |

|---|---|---|---|

| 2001 | Direct obligations, Cat A | $75,000,000 | |

| 2002 | Direct obligations, Cat B | $15,000,000 | |

| 2190 | Total obligations | $90,000,000 | 75% |

| 2201 | Apportioned, available current | $5,000,000 | |

| 2202 | Apportioned, available subsequent | $20,000,000 | |

| 2490 | Unobligated balance | $30,000,000 | 25% |

| 2500 | Total budgetary resources | $120,000,000 | 100% |

This agency has:

- Obligated 75% of their resources through Q3

- 4% remaining in current-period apportionment ($5M in 2201)

- 17% apportioned for Q4 ($20M in 2202)

- No deferrals, no rescissions (lines 2401-2402 = $0)

That's a healthy execution profile. They're spending on pace without burning through resources too fast.

What an Unhealthy Account Looks Like

| Line | Description | Amount | Problem |

|---|---|---|---|

| 2001 | Direct obligations, Cat A | $30,000,000 | |

| 2190 | Total obligations | $30,000,000 | Only 25% obligated by Q3 |

| 2201 | Apportioned, available current | $60,000,000 | $60M just sitting there |

| 2402 | Withheld pending rescission | $20,000,000 | Funds being held back |

| 2490 | Unobligated balance | $90,000,000 | 75% unobligated |

| 2500 | Total budgetary resources | $120,000,000 |

This agency has:

- Obligated only 25% of resources through Q3 (behind pace)

- $60M apportioned but unused (execution problem)

- $20M withheld by executive action (political hold)

- 75% of the year's resources still sitting unobligated

That's a troubled account. Either the agency can't spend the money (program problems), or someone is stopping them (political constraints).

SF-132 to SF-133: The Comparison

Here's how to compare plan to actuals:

| Question | SF-132 Shows | SF-133 Shows | Comparison Reveals |

|---|---|---|---|

| How much was apportioned by quarter? | Lines 6001-6004 | Line 2001 | Pace: Are they on track? |

| How much for each program? | Lines 6011-6159 | Line 2002 detail | Priorities: Right programs? |

| What's being held back? | Lines 6180-6181 | Lines 2401-2402 | Politics: Executive holds? |

| Total apportioned vs obligated | Line 6190 | Line 2190 | Execution: Using what's allowed? |

The SF-132 is the speed limit. The SF-133 shows how fast you're actually going. The gap between them tells the execution story.

The Bottom Line

Section 2XXX answers: What did the agency do with the money?

Key takeaways:

- Lines 2001-2003: Direct obligations by Category A, B, or exempt

- Lines 2101-2103: Reimbursable obligations (interagency work)

- Line 2190: Total new obligations

- Lines 2201-2203: Apportioned balances still available

- Lines 2401-2403: Unapportioned—including deferrals and rescissions

- Line 2500 must equal Line 1910 (the balance check)

- Obligations > Apportionments = potential ADA violation

The 2XXX section is where accountability lives. It's where you find out if the plan matched reality.

What's Next

We've covered what agencies had (Section 1) and what they committed (Section 2). But commitments aren't cash. An obligation is a promise to pay—it's not money out the door.

In Part III, we'll cover Section 3XXX: Outlays. This is where obligations become payments, and the full lifecycle of a federal dollar completes.

BlazingStar Analytics is building real-time budget execution tracking that connects appropriations, apportionments, and SF-133 reports. Get early access to our platform, launching Spring 2026.