What is an SF-133?

The apportionment told the agency what it could spend. The SF-133 tells you what actually happened.

1. What is an SF-133?

2. How to Read an SF-133, Part I: Budgetary Resources (1XXX Lines)

3. How to Read an SF-133, Part II: Status of Budgetary Resources (2XXX Lines)

4. How to Read an SF-133, Part III: Outlays (3XXX Lines)

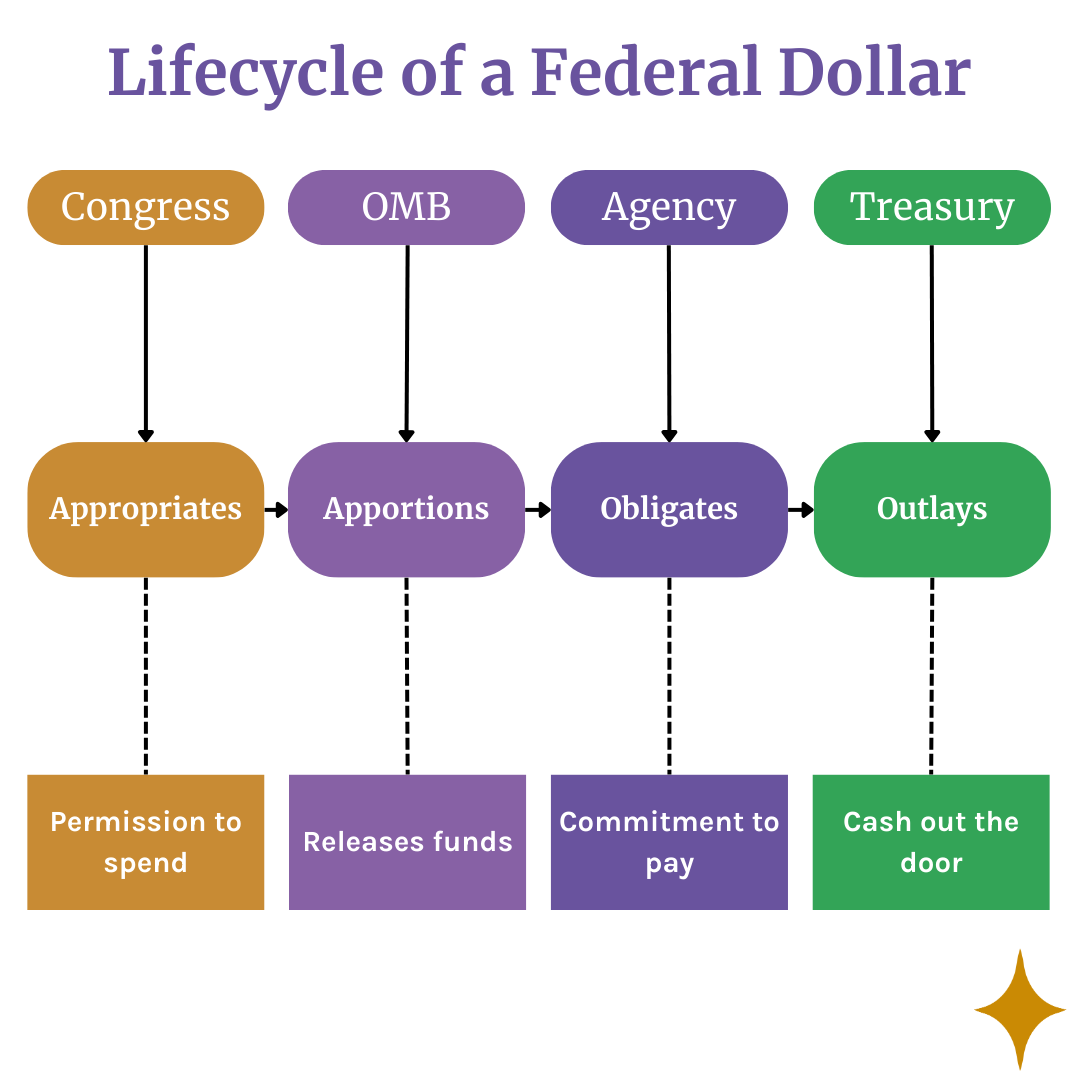

If you've been following this blog, you know the federal spending lifecycle: appropriation, apportionment, obligation, outlay. Congress provides authority. OMB releases funds. Agencies commit dollars. Treasury pays bills.

But how do you know if any of that actually happened?

That's where the SF-133, or Report on Budget Execution and Budgetary Resources comes in. It's the federal government's quarterly report card on budget execution—the document that shows what agencies actually did with the money they were given. This series is timely—last week (January 5, 2026) OMB published the first set of SF-133 data for Fiscal year 2026.

The 60-Second Version

| Term | What It Means | Restaurant Analogy |

|---|---|---|

| SF-133 | Quarterly execution report submitted to Treasury/OMB | Your itemized receipt |

Key insight: The apportionment is the plan. The SF-133 is the actuals.

- SF-132 (apportionment) = What you decided to spend tonight

- SF-133 = What you actually ordered, ate, and paid for

Same line numbers. Same structure. Different purpose. One looks forward (what can be spent), the other looks backward (what was spent).

Until you compare the two, you don't really know if the plan matched reality.

Click here for a quick visual explainer.

Key Resources

These two documents are the heavy hitters for learning the ins and outs of the SF-133:

I'll be honest. These documents are deeply technical and aren't really accessible unless you've worked in government. Heck, I doubt that most Hill staff have waded into these waters. But, if you interested in learning more about the pace and timing of federal obligations and outlays, there's no better source than the SF-133. It's worth the effort and the reason for this series.

Why the SF-133 Exists

Agencies don't just spend money and hope someone notices. Federal law requires them to report their execution to Treasury and OMB every quarter.

The legal authority comes from 31 U.S.C. § 1511-1514, which requires agencies to report obligations and expenditures. These reports feed into government-wide financial statements and tell Congress and OMB whether agencies are following the spending plan.

Translation: The SF-133 is how the government keeps score.

Where SF-133 Fits in the Lifecycle

Remember the lifecycle of a federal dollar?

| Stage | Document | What It Shows |

|---|---|---|

| Appropriation | Appropriations Act | Congress authorized spending |

| Apportionment | SF-132 | OMB released funds to the agency |

| Obligation | SF-133 | Agency obligated the money |

| Outlays | SF-133 | Money went to recipients |

The apportionment is the speed limit. The SF-133 is the speedometer.

If you want to know whether an agency is spending on pace, on the right things, or at all—the SF-133 is your primary source.

The Restaurant Analogy: The Receipt

We've been using a restaurant metaphor throughout this series. Here's how the SF-133 fits:

-

Appropriation: You have $250 in your wallet when you sit down. That's your budget authority.

-

Apportionment: You decide you'll only spend $100 tonight. You're keeping $150 in reserve.

-

Obligation: You order the steak ($45). You've committed to pay.

-

SF-133: The itemized bill at the end of the night—showing what you ordered, what you paid, and what's left in your wallet.

The SF-133 closes the loop. It's the receipt that proves what actually happened.

Relationship to the Apportionment (SF-132)

Here's where it gets interesting: the SF-133 and SF-132 use the same line number structure.

| Line Series | SF-132 (Apportionment) | SF-133 (Execution) |

|---|---|---|

| 1XXX | Budgetary resources available | Budgetary resources that materialized |

| 2XXX | — | Status of those resources (obligations, balances) |

| 6XXX | How resources are apportioned | — |

| 3XXX | — | Outlays (actual payments) |

The SF-132 tells you what OMB authorized. The SF-133 tells you what actually occurred.

Comparing them reveals the execution story:

- Did the agency obligate what OMB allowed?

- Did they spend faster or slower than planned?

- Did collections come in higher or lower than estimated?

- Is money sitting unobligated that should be moving?

This comparison is the core of budget execution analysis.

A Real Example

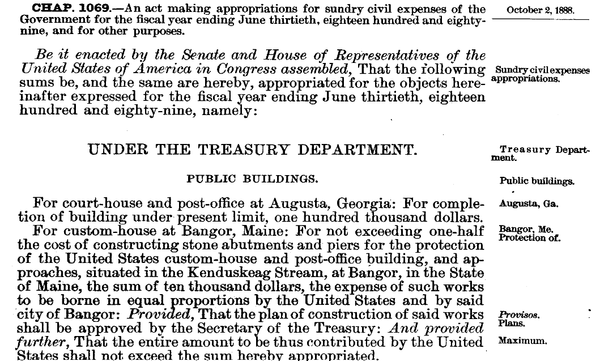

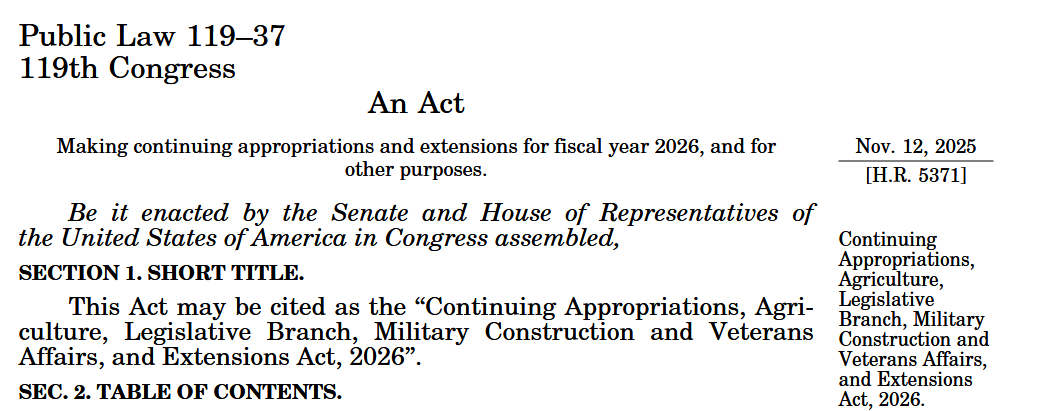

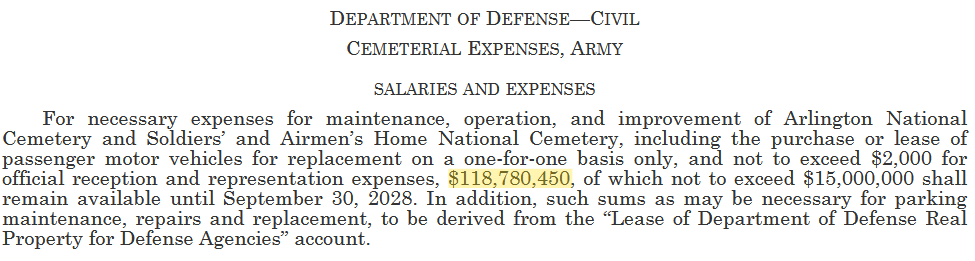

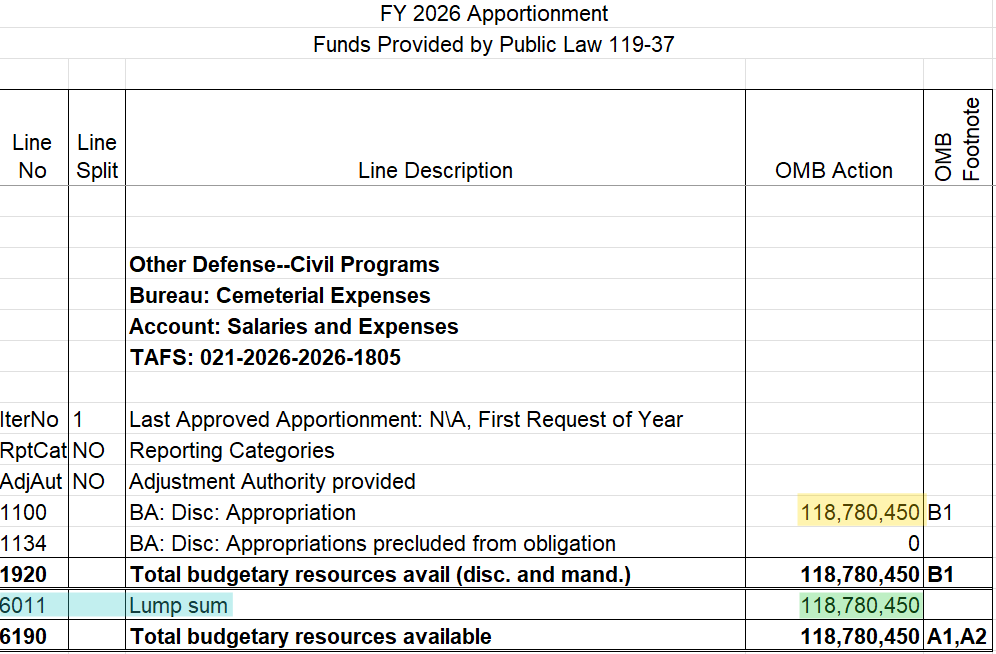

Let's trace an example from the appropriation through the apportionment and the SF-133. Below, you'll find the appropriation for the salaries and expenses account that funds the maintenance and upkeep of Arlington National Cemetery and the Soldiers’ and Airmen’s Home National Cemetery from the 3-bill minibus and continuing resolution through January 30, 2026 (P.L. 119-37).

Source: H.R.5371 - Continuing Appropriations, Agriculture, Legislative Branch, Military Construction and Veterans Affairs, and Extensions Act, 2026

Note the appropriated amount of $118,780,450, highlighted in yellow. OMB apportioned those funds here:

Source: Apportionment for 021-1805 /2026 - Salaries and Expenses, Nov 25, 2025: OMB | OpenOMB

You'll see that Line 1100, $118,780,450, matches the appropriated amount. OMB made the entire $118,780,450 available in a lump sum on line 6011. It's a pretty straightforward apportionment with few moving parts.

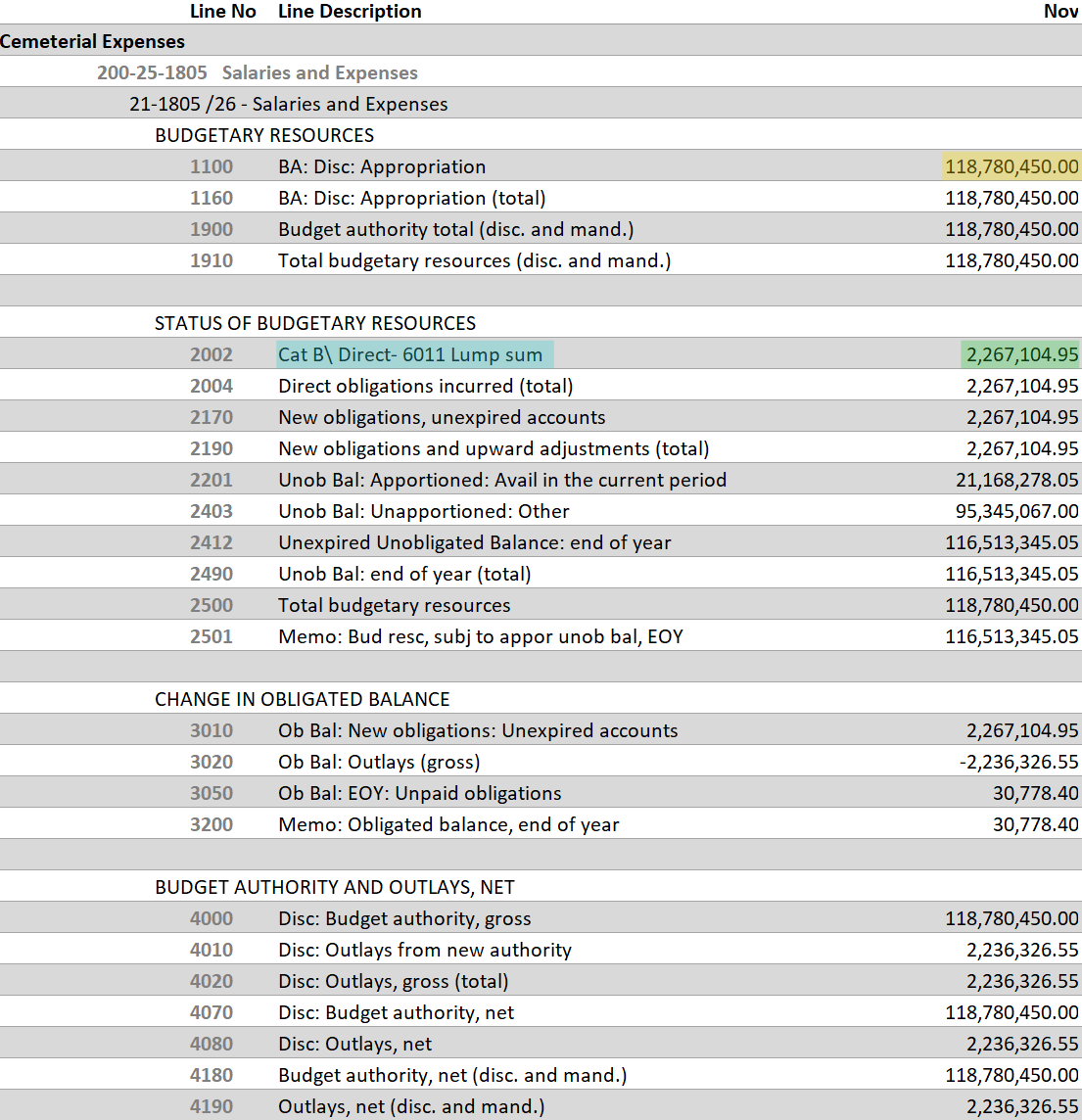

Now let's take a look at the SF-133 for the account for November 2025. A quick note, SF-133s are available monthly, but there is a lag. Fiscal year end closeout is demanding and there was a shutdown during this time period. That said, OMB released the November SF-133 data on January 5, 2026. It won't usually be that long of a delay. Typically reports are made public 3 or 4 weeks after the end of the reporting month.

Source: FY 2026 - SF 133 Reports on Budget Execution and Budgetary Resources, Other Defense Civil Programs

First, I want to get you situated. At the top of the SF-133 we have:

- the bureau name, "Cemeterial Expenses",

- account name, "Salaries and Expenses" and

- the TAFS: "21-1805 /26".

Note that the bureau and account names match exactly, but the TAFS is in a slightly different format: "021-2026-2026-1805". That's expected. We covered the different TAFS formats in an earlier post.

The TAFS: The Universal Identifier for Federal Spending

Appropriations, Obligations, and Outlays: The Three Stages of Federal Spending

The SF-133 has pretty well-organized sections.

| Section | Lines | What it shows |

|---|---|---|

| Budgetary Resources | 1XXX | The funds that make up this TAFS |

| Status of Budgetary Resources | 2XXX | Are the funds available, how much has been obligated, how much is remaining |

| Change in Obligated Balance | 3XXX | A running total of what's been obligated, what's been paid out, and how much is left |

| Budget Authority and Outlays, Net | 4XXX | This section is a recap of the first 3 sections |

| Memo Lines | 5XXX | This summarizes information in the first four sections |

Looking at the apportionment for Cemeterial Expenses,

Budgetary Resources Section, Lines 1100-1910 show the budgetary resources that actually materialized:

- Appropriation received (1100, 1160): $118,780,450

- Total resources available (1900, 1910): $118,780,450

You can see that Line 1100 on the SF-133, $118,780,450 also matches line 1100 from the apportionment document and both are highlighted in yellow. You're probably asking yourself: "Why are all of these numbers repeated so much?" This will make sense when we get to a more complicated account with mandatory and discretionary funds, or transfers or collections.

Status of Budgetary Resources, Lines 2002-2501 show the status of those resources:

- Obligations incurred (2002, 2004, 2170, 2190): $2,167,104.95

- Unobligated balances (2412, 2490): $116,513,345

- Total budgetary resources (2500): $118,780,450

I want to draw your attention to a few things. First, note that line 2002, highlighted in blue, refers back to line 6011 on the apportionment. This is a great example of the speed limit (apportionment) and speedometer (SF-133) analogy. OMB apportioned $118,780,450 for the year. Army obligated $2,167,104.95 in the month of November, 2025.

Second, note that lines 1910 and 2500 equal each other. That's a key check here, just like on the apportionment document.

Change in Obligated Balance, Lines 3010-3200 show the amount of funds actually outlayed (funds left Treasury):

- New obligations this month (3010): $2,167,104.95

- Outlays made this month (3020): -$2,236,326.55

- Unpaid Obligations (3050): $30,778.40

Note that line 3010 and 2190 are equal.

I want to note the presence of the Budget Authority and Outlays section. It summarizes the information above. There's also a memo section, that I omitted. These two sections summarize and repackage information contained in the previous two sections. We'll cover how to use those later in the series.

So, to go back to the restaurant analogy:

| Section | Lines | Restaurant Analogy |

|---|---|---|

| Budgetary Resources | 1XXX | Funds in your wallet |

| Status of Budgetary Resources | 2XXX | Ordered the meal |

| Change in Obligated Balance | 3XXX | Paid the check |

The posts for the next three weeks will cover these sections in detail.

Where to Find SF-133s

Unlike apportionments, SF-133 data isn't as easily browsable. Here's where to look:

MAX.gov (Agency Submissions)

Agencies submit SF-133s through MAX.gov.

This page, SF 133 Report on Budget Execution and Budgetary Resources, has links to fiscal years, and then the fiscal years link to agencies. For example, this page has SF-133 data for Fiscal year 2026.

USAspending.gov

USAspending draws on SF-133 data for its account-level summaries. It's not the raw SF-133, but it's often more accessible for quick lookups.

Note on Accessibility

SF-133s are less accessible than apportionments for a reason: they're primarily internal management documents. Apportionments became public partly due to political interest in slowed spending and policy conditions. SF-133s don't have the same profile—but they should.

Why Should You Care?

If you're tracking federal spending, the SF-133 answers questions that appropriations and apportionments can't:

"Congress appropriated $500 million. OMB apportioned $400 million. What did the agency actually obligate?"

The SF-133 tells you. Maybe they obligated $380 million. Maybe $200 million. The execution report shows reality.

"Is this program spending on pace?"

Compare quarterly SF-133s to the quarterly apportionment schedule. If Q2 obligations are far below Q2 apportioned amounts, they're behind. You can also compare monthly SF-133 data across multiple fiscal years. There's at least some quarterly SF-133 data available back to 1998, and monthly data from 2013 onward. Even if you wanted to limit yourself to the easiest to use SF-133 data 2018-onward, that's still more data than apportionments which first became publicly available in 2022.

"Why is there money left over at year end?"

The SF-133 shows unobligated balances and their status—available, unavailable, expired. You can see whether money lapsed because the agency couldn't spend it or because something blocked them.

"Is the apportionment constraint or is the agency slow?"

If apportionment is high but SF-133 obligations are low, it's an agency execution issue. If both are low, the constraint is likely upstream at OMB.

"How can I find out about spending in the Legislative or Judicial Branch?"

Federal law only requires that Executive branch apportionments are made public. However, both the Legislative and Judicial branches submit SF-133 data.

The Bottom Line

- Apportionment (SF-132) = permission

- SF-133 = reality

- The gap between them = where oversight happens

The SF-133 is the execution report that proves whether federal spending matched the plan. Without it, you're guessing.

| Feature | SF-132 (Apportionment) | SF-133 (Execution) |

|---|---|---|

| Frequency | As needed (at least once a year) | Monthly |

| Focus | Future (Authority) | Past (Activity) |

| Key Question | "How much can we spend?" | "How much did we spend?" |

Key takeaways:

- SF-133 is the quarterly execution report submitted to Treasury/OMB

- Same line structure as SF-132, different purpose (actuals vs. plan)

- Comparing SF-132 to SF-133 reveals execution performance

- Essential for tracking whether agencies are spending on pace and on purpose

What's Next

Now that you know what an SF-133 is and why it matters, you're ready to learn how to read one. In our next post, we'll start with the top section: Budgetary Resources (1XXX lines)—where the money comes from.

BlazingStar Analytics is building real-time budget execution tracking that connects appropriations, apportionments, and SF-133 reports. Get early access to our platform, launching Spring 2026.