CSBAs, Detail Tables, and You

The House Energy & Water Development mark just came out as H. Rept. 119-667. Most people will read the directives and the narrative. The pros flip to the back first — to a single table that tells you, account by account, exactly what happened. Let's get into it.

The 60-Second Version

| Question | Answer |

|---|---|

| What is it? | The Comparative Statement of New Budget (Obligational) Authority — the account-by-account table comparing last year's enacted level, the President's request, and the Committee's recommendation |

| Where does it live? | The back matter of the committee report (here: H. Rept. 119-667) |

| What's the unit? | Budget authority, in thousands of dollars — not outlays, not whole dollars |

| Why care? | One table shows every funding change, and every fight, in the bill |

| The catch? | It only exists once the report is filed — there's a lag from when the bill is first marked up |

Key insight: The bill text gives you ceilings. The CSBA gives you the whole story — what moved, by how much, against two different baselines — for every account in the bill, all in one place. It is the single most useful table in the appropriations paper trail, and almost nobody outside the process reads it.

A quick naming note before we go further: in the world of appropriations, "CSBA" is shorthand for the Comparative Statement of (New) Budget Authority. That's what we mean every time we say CSBA in this post.

Pro Tip: I will never refer to this document as a C-S-B-A. I call it a "ciz-buh". If you're a casual observer, you'll rarely hear it aloud. But for a former committee staffer like me, every time I type or read CSBA, I hear "ciz-buh" in my head.

What the CSBA Is — and Where It Lives

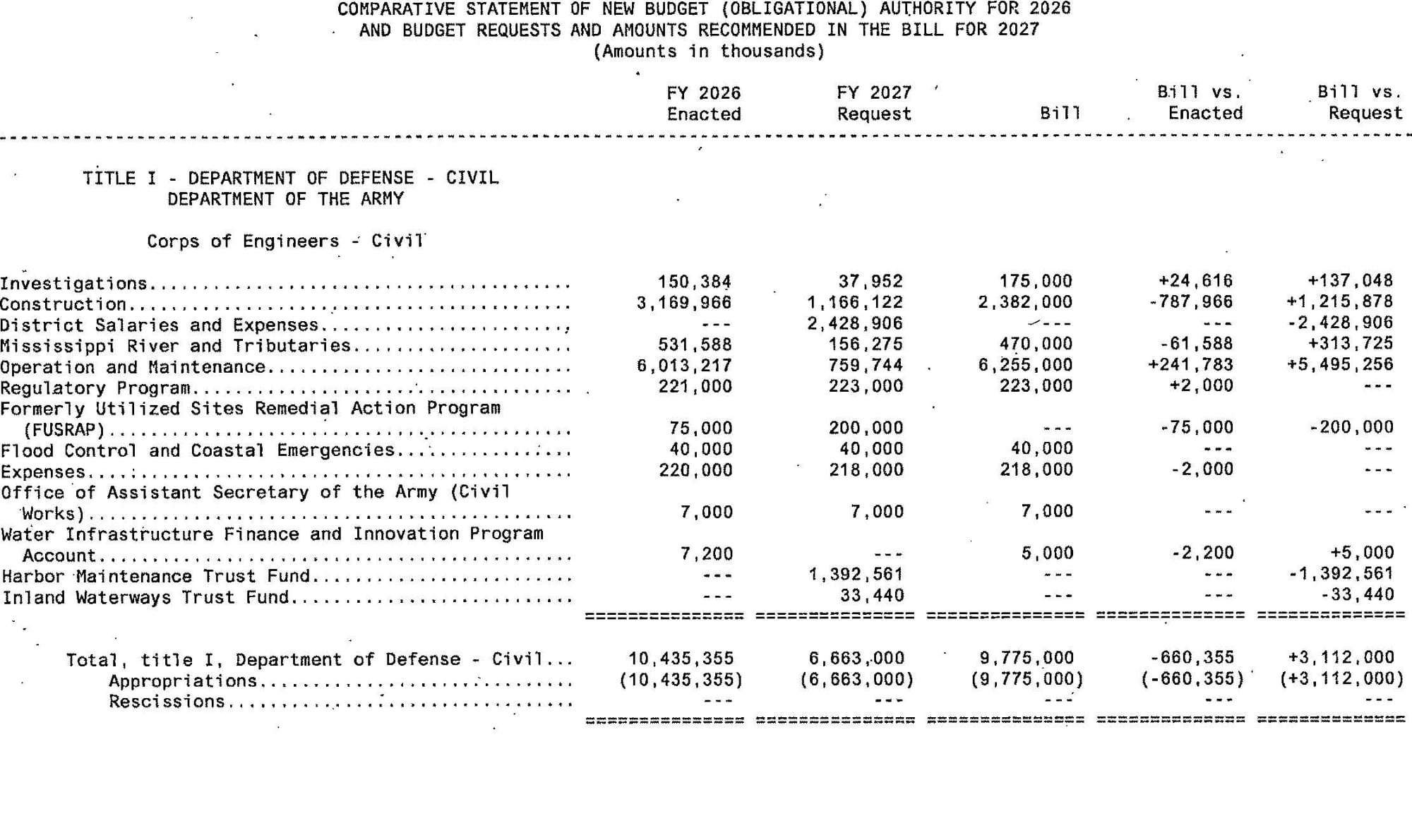

When a subcommittee finishes a bill, the Committee files a report to accompany it. That report has narrative, it has directives to agencies, and — at the very back — it has tables. The biggest and most important of those is the Comparative Statement of New Budget (Obligational) Authority.

It's a comprehensive ledger of the entire bill. Every account in the subcommittee's jurisdiction gets a row. For Energy & Water, that means the Army Corps of Engineers, the Bureau of Reclamation, the entire Department of Energy (including NNSA, the Office of Science, and the applied-energy programs), and the independent agencies like the Nuclear Regulatory Commission. All of it, on one running table.

Don't confuse the CSBA with two things that look like it:

- The summary table in the front of the report ("bill totals") — that's a high-altitude topline, a handful of rows.

- The project-level tables scattered through the account narratives — those drill below the account level for specific accounts. We'll cover these project-level or detail tables later on.

The CSBA sits between them: every account, at the account (and key sub-account) level, comparing three numbers.

Translation: The bill text tells you how much. The CSBA tells you how much compared to what — and it does it for the whole bill at once.

One more thing, and it trips up everyone the first time: the CSBA is in thousands of dollars. A line that reads 8,500,000 is $8.5 billion, not $8.5 million. The column headers say so, usually once, at the top. If your number feels off by three orders of magnitude, it is.

Reading the Columns

We'll be referring to the 2027 Energy and Water Report, H. Rept. 119-667, throughout this post.

The standard House layout reads left to right:

- Item — the account, agency, or program name, indented to show hierarchy (title → agency → account → line item).

- FY [prior] Enacted — the current-law baseline. Where you are today.

- FY [current] Budget Request — the President's ask. (This is the number that came out of the Budget Appendix we covered earlier — the request finally meets Congress here.)

- Bill — what this bill does.

- Bill vs. Enacted

- Bill vs. Request

The recommendation column is the bill. The other two columns are reference points — they exist so you can measure the recommendation against something.

The indentation is load-bearing. Sub-account lines roll up into account totals, account totals roll up into agency totals, agency totals roll up into the title total, and the titles roll up into the grand total at the very bottom. When you're not sure what level you're reading, trust the indentation.

Here's what the first page of the CSBA in H. Rept. 119-667 looks like:

The Three Comparisons That Matter

Here's why this is the most useful table in the bill. With three numbers in each row, you get three subtractions — and each one tells a different story.

- Recommendation − Enacted = the policy change. Up, down, or flat against current law. This is the headline: did this program grow or shrink?

- Recommendation − Request = how Congress treated the President. Did the Committee honor the ask, ignore it, or actively reject it? This is where you see who won.

- Enacted vs. Request = the size of the ask. What the President wanted to change before Congress weighed in.

Key insight: The gap between the Request column and the Recommendation column is where the politics lives. A program the President wanted to zero out, restored by the Committee. A requested increase the Committee declined to fund. A plus-up the President never asked for. You can read the entire negotiating posture of a subcommittee just by scanning those two columns against each other.

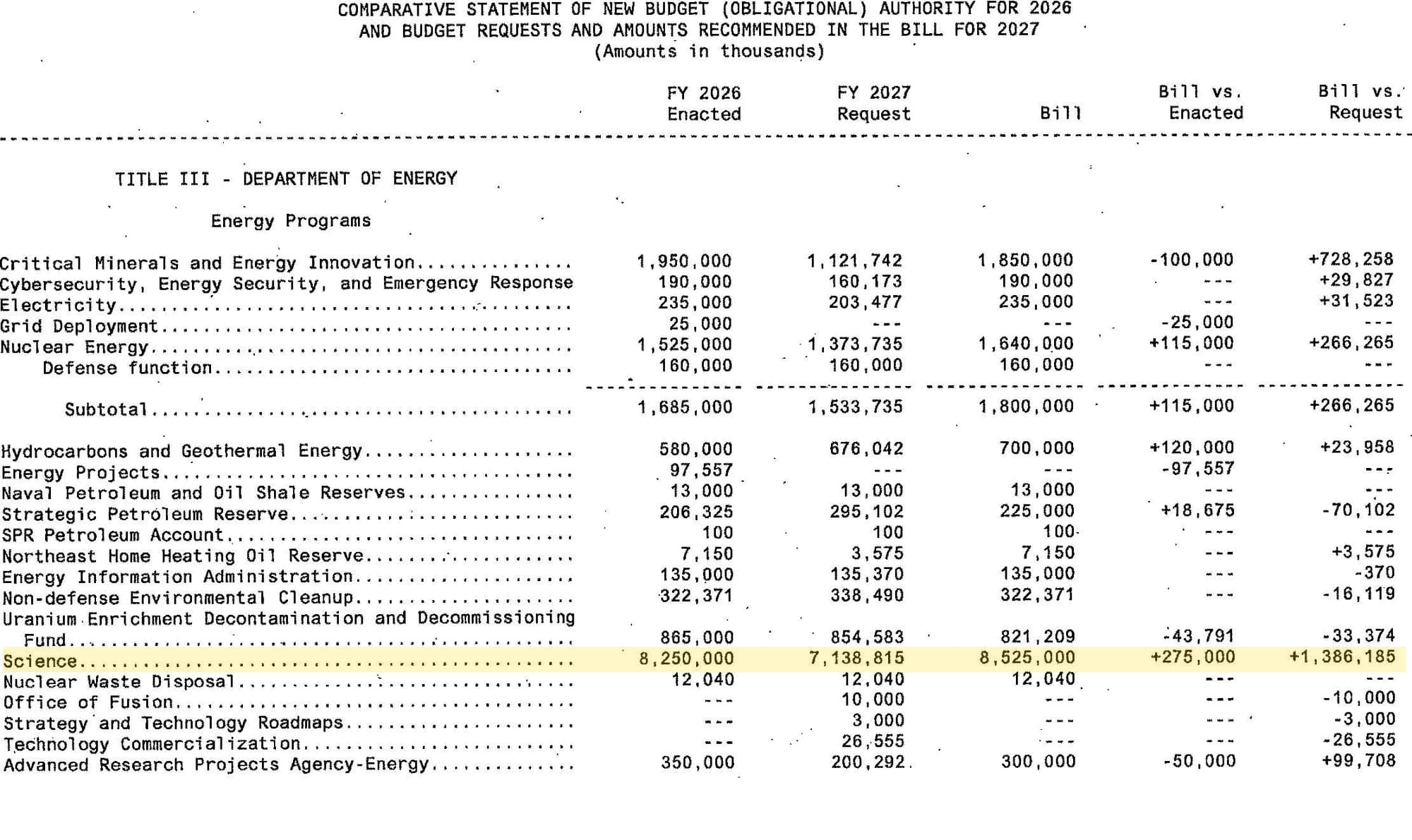

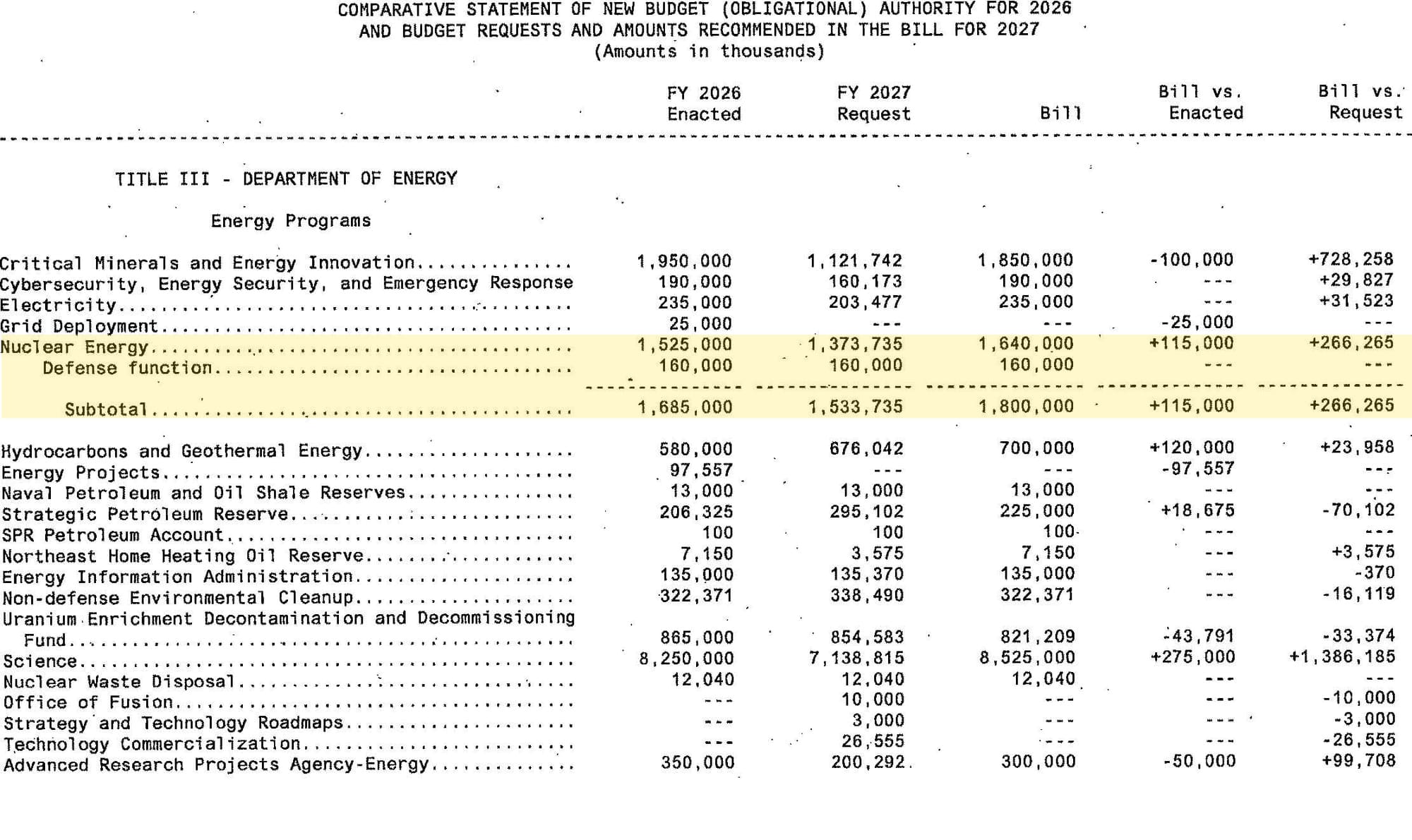

Consider Department of Energy—Science, highlighted below:

The President's request proposed $7.1 billion, a $1.1 billion cut from the FY 2026 enacted level. The FY 2027 House E&W mark funds Science at $8.5 billion, a $275 million increase over enacted and $1.4 billion above the request.

But continuing down the CSBA, you get a flavor of the dynamics. Nuclear Waste Disposal is flat with both the request and enacted. The request included $10 million for a new Office of Fusion account; the mark didn't fund it.

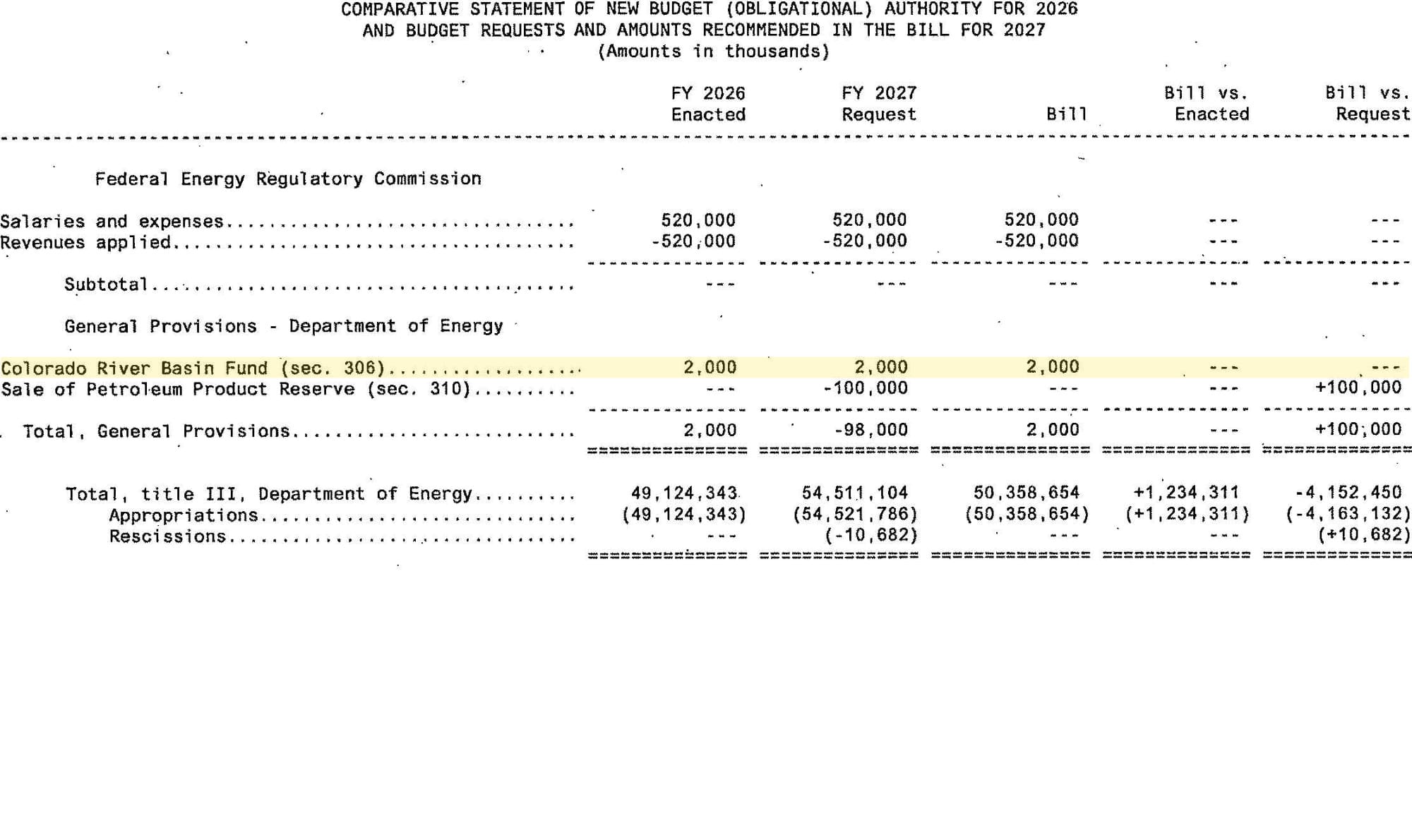

When a Provision With No Dollar Amount Has a Cost

This is the example that converts people.

Most of what you read in an appropriations bill comes with a number attached. But the general provisions — the "Sec. 301, Sec. 302…" section near the back of the bill — are often pure legislative language. No dollar figures. Just rules. And it is easy to read right past them as if they're free.

They're not. Watch:

Sec. 306. No funds shall be transferred directly from "Department of Energy—Power Marketing Administration—Colorado River Basins Power Marketing Fund, Western Area Power Administration" to the general fund of the Treasury in the current fiscal year.

Read the text. There is not a single dollar amount in it. It's a prohibition — Congress is saying money may not move from this fund to the Treasury's general fund this year.

But that transfer would have been money coming in — an offsetting receipt that reduces the cost of the bill. Block it, and the bill just got more expensive by exactly the amount that won't flow to Treasury. The scorekeepers catch this even though the drafter wrote no number.

So where does the number show up? The CSBA. That's the first place — often the only place — you'll see this provision carries a price:

2,000 — in thousands — is $2 million. A provision with zero dollar amounts in its text scores at $2 million, and the comparative statement is where that cost becomes visible.

Translation: Bill language without a number is not the same as bill language without a cost. The CSBA is your early-warning system for the provisions whose price tag is hidden in the prose.

The Other Tricky Bits

A few more things that trip people up:

- Zero versus blank. A

0or---in the recommendation column means a proposed termination or no funding this year. A blank usually means the line didn't exist in that year's structure. Don't read them as the same thing. - Negative numbers. Rescissions, offsets, and changes in mandatory programs (CHIMPs) show up as negatives. A number in parentheses or with a minus sign isn't a typo — it's money being pulled back or scored as a savings. Many credit programs or fee funded programs will have large negative numbers — those are revenue generators for that bill.

- Comparability footnotes. When account structures change — a transfer, a consolidation, a realignment — the prior-year columns get restated so the comparison is apples-to-apples. A line can appear to move year-over-year simply because the furniture got rearranged. The report text usually tells you when that's happened.

- Emergency and cap-adjustment designations. Money designated as emergency, disaster, or a cap adjustment breaks a naive year-over-year read. Watch for the flags.

- Budget authority is not outlays. The CSBA is budget authority only. With multi-year and no-year money, the authority granted this year and the money that actually flows this year are different things.

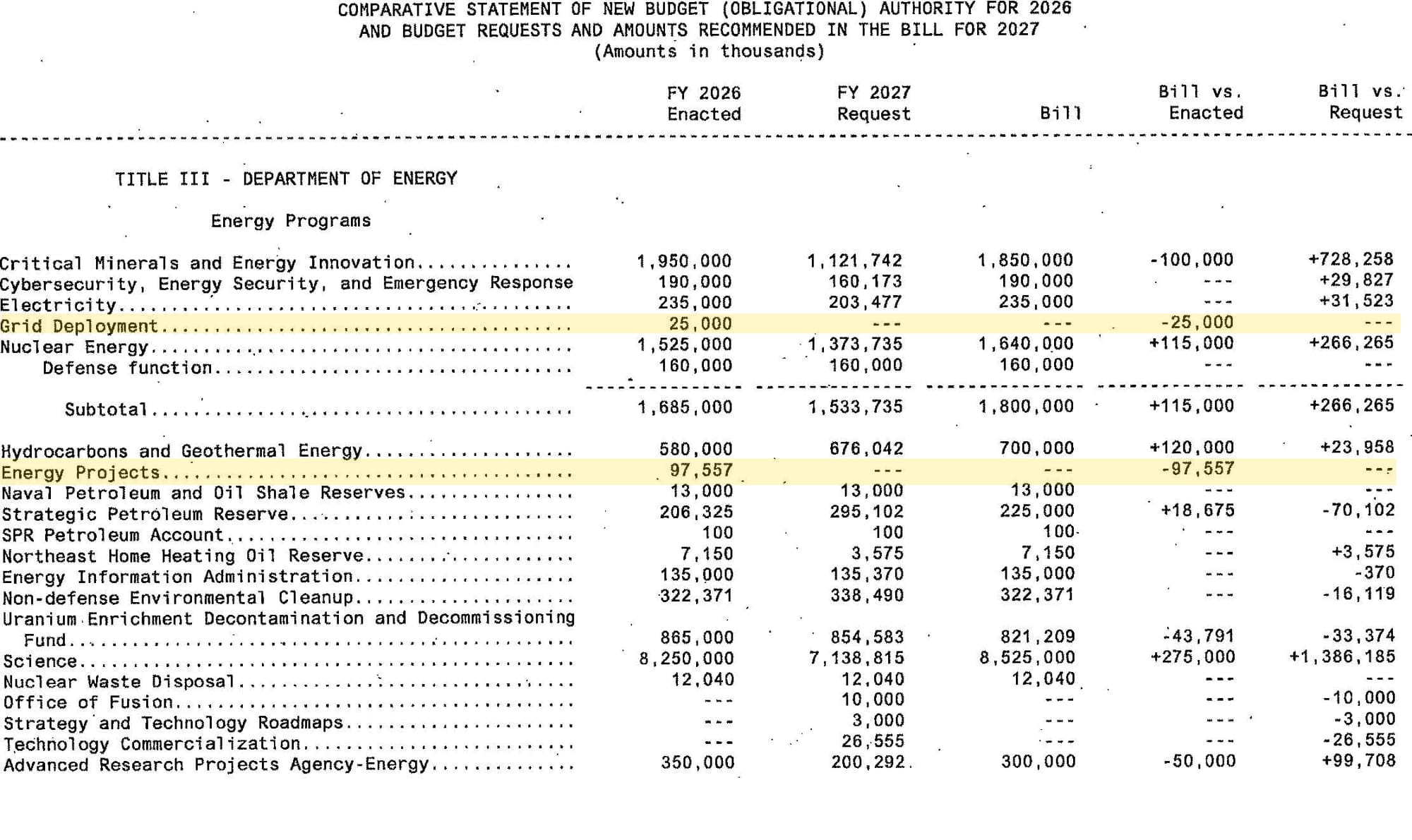

Let's look at some examples of these. Let's say your boss tells you to track two specific accounts: Grid Deployment and Energy Projects. You're eager, you read the bill, you come up empty. You download the bill again because you think there's an error — you know it got funding last year. You still can't find it. Take a look at the table:

On the CSBA, you can see that, indeed, both Grid Deployment and Energy Projects received funding last year, but the President requested $0, shown here as "---" and the House took him up on it. You weren't being gaslit, they just eliminated the program.

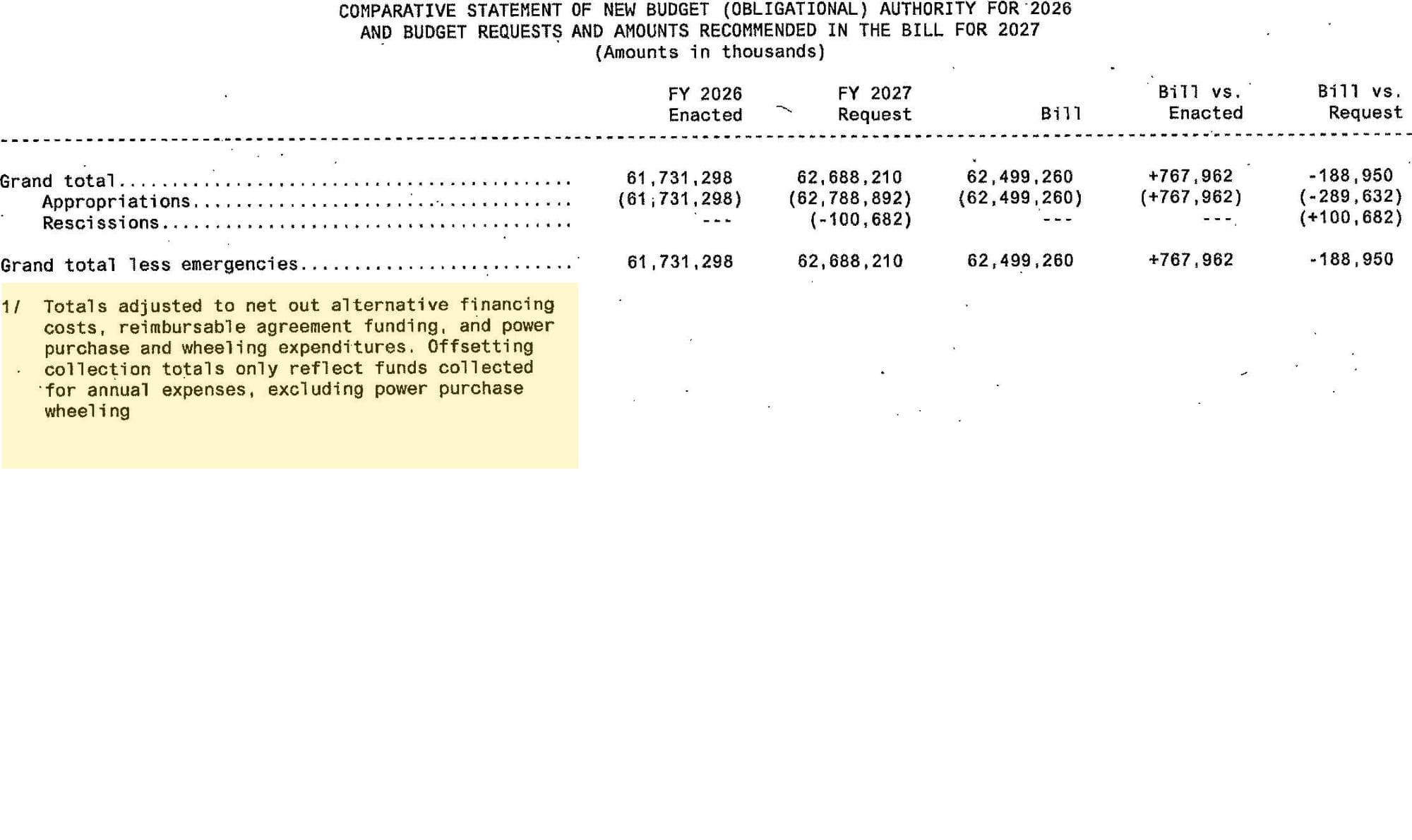

Our next example is a little more ministerial. There's a footnote at the end of the CSBA. The Energy and Water Bill includes entities like the Tennessee Valley Authority and Bonnevile Power Administration that generates, purchases, and sells power. They behave like a utility. So, this footnote tells you that they've taken this into account and adjusted the figures to account for this difference in fiscal operations.

Reconciling the CSBA to Everything Else

The CSBA doesn't live in isolation — it has to tie out.

- The grand total reconciles to the bill's total and to the subcommittee's 302(b) suballocation.

- Each account row reconciles to the corresponding account paragraph in the bill text.

- For accounts with project-level detail, the account total reconciles to the project tables in the report narrative.

So you can triangulate any single account across three documents: the bill text (the legal ceiling), the CSBA (the comparison), and the project table (the detailed plan). When they all agree, you understand the account. When they don't, you've found either a footnote you missed or a story worth chasing.

Translation: If the CSBA, the bill, and the project tables disagree, that's not noise. That's a lead.

A note on legal force, since people ask: the CSBA is the Committee's recommendation. At the House-report stage, it's not law — it's the comparison that travels with the bill. But report tables don't always stay advisory. Sometimes the bill text itself reaches back and gives a report table the force of law — and we're about to see exactly that in the next section. (We touched on incorporation by reference in the Reports post; it deserves its own deeper treatment, and we'll give it one.)

Worked Example: Nuclear Energy, End to End

Let's run a single account from H. Rept. 119-667 through the whole machine. We'll use Nuclear Energy, because the Administration and Congress had a real disagreement here — and because its bill text shows the report table doing something most people don't know report tables can do.

Here's the account paragraph from the bill:

Nuclear Energy

For Department of Energy expenses including the purchase, construction, and acquisition of plant and capital equipment, and other expenses necessary for nuclear energy activities in carrying out the purposes of the Department of Energy Organization Act (42 U.S.C. 7101 et seq.), including the acquisition or condemnation of any real property or any facility or for plant or facility acquisition, construction, or expansion, $1,800,000,000, to remain available until expended: Provided, That of such amount, $92,000,000 shall be available until September 30, 2028, for program direction: Provided further, That for the purpose of section 954(a)(7) of the Energy Policy Act of 2005, as amended, the only amount available shall be from the amount specified as including that purpose in the "Bill" column in the "Department of Energy" table included under the heading "Title III—Department of Energy" in the report accompanying this Act.

Now walk it through:

1. Find it in the CSBA. Nuclear Energy sits under Title III — Department of Energy. Read the numbers (thousands, as always):

The recommendation is 1,800,000 — that's $1.8 billion. Note how the account is split in two: Nuclear Energy, a Defense function, and an account subtotal. That's because the 302(b) allocations for the subcommittee are subdivided into defense and non-defense. The $160 million for defense is charged separately from the $1.6 billion of non-defense funding.

2. Look at the comparisons.

- Rec − enacted — the policy change vs. current law. The request proposed a cut of $151 million from the FY 2026 level.

- Rec − request — this is the story. This is where the Administration and Congress diverge. The House mark wants to increase the account by $115 million above the enacted level.

3. Read the provisos — the bill carves up the account before you ever leave the page. The first proviso fences $92 million for program direction and stretches its availability to September 30, 2028. So $1.8 billion total, but a slice is earmarked and given a longer runway.

4. Watch the second proviso give a report table the force of law. Read it again: for the section 954(a)(7) purpose, the only amount available is whatever appears in the "Bill" column of the "Department of Energy" table in the report.* The statute has a percentage based set-aside. Here's the text of 954(a)(7):

(7) Nuclear energy university program

In carrying out the programs under this section, the Department shall, to the maximum extent practicable, allocate 20 percent of funds appropriated to nuclear energy research and development programs annually, excluding funds appropriated for the Advanced Reactor Demonstration Program of the Department, to fund university-led research and university infrastructure projects through an open, competitive solicitation process.

My crude math (not knowing if the entire account consists of nuclear energy research and development programs) indicates that 20 percent of $1.8 billion is $360 million. Instead, the bill points at the table and says that number, not the percentage, is the legal limit.

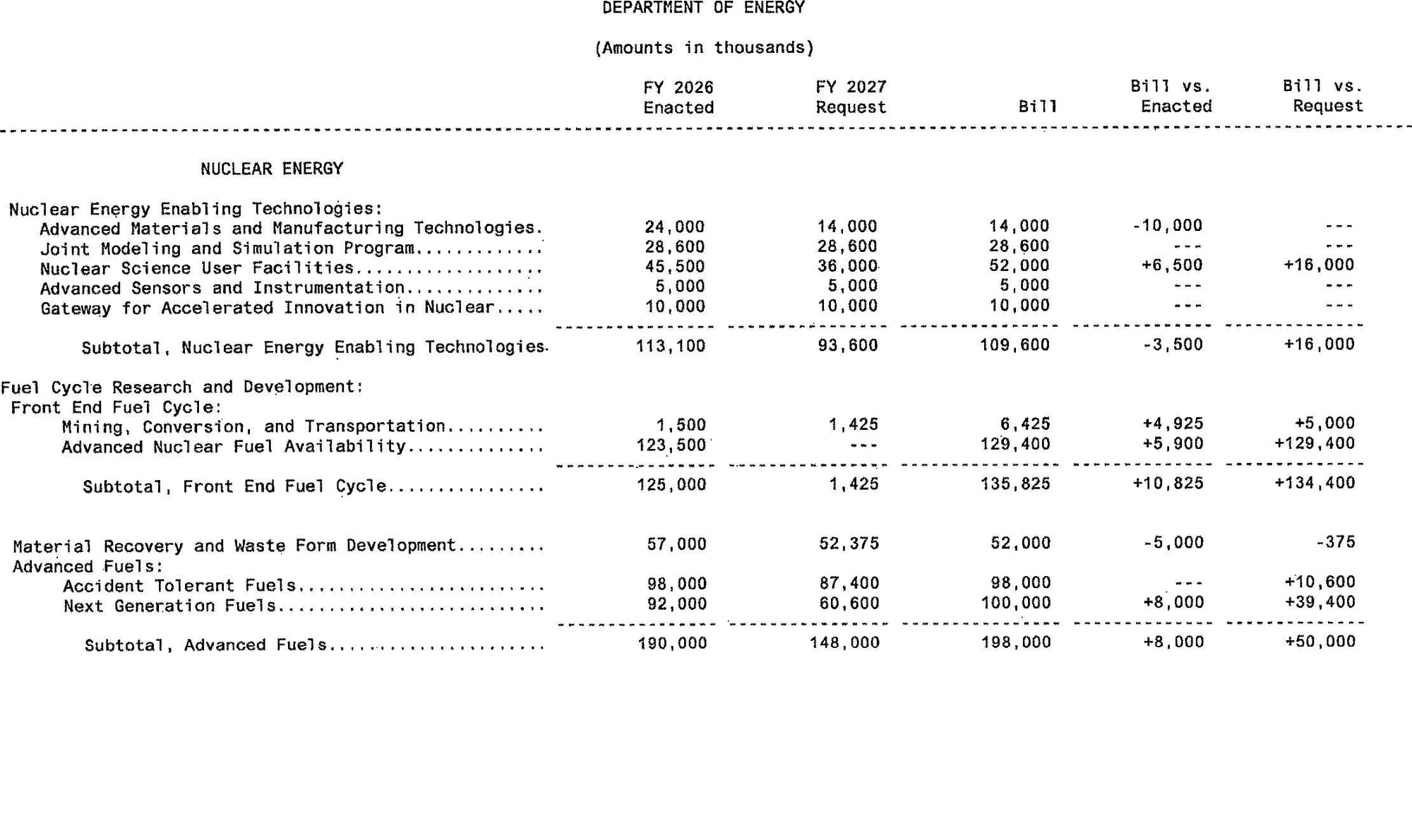

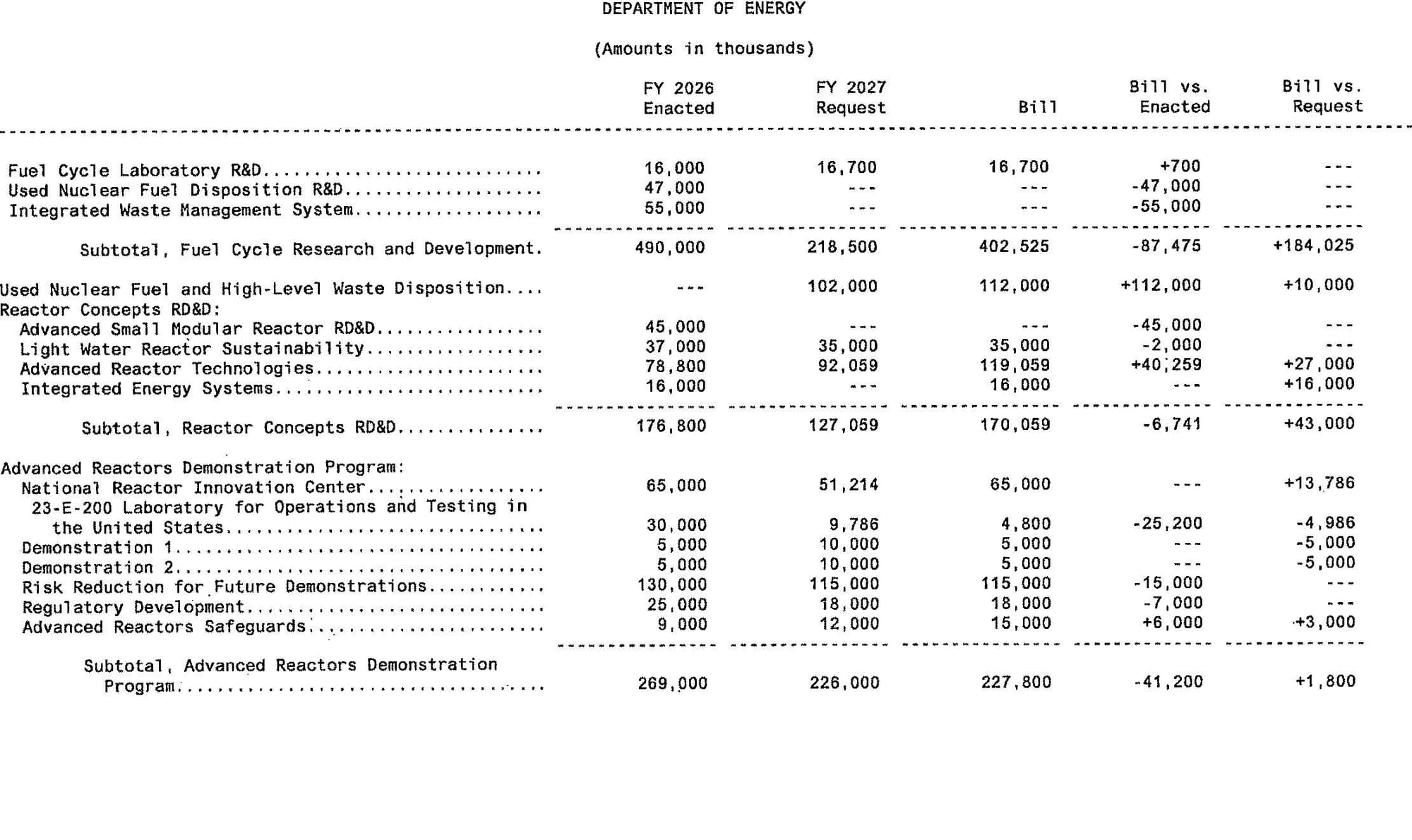

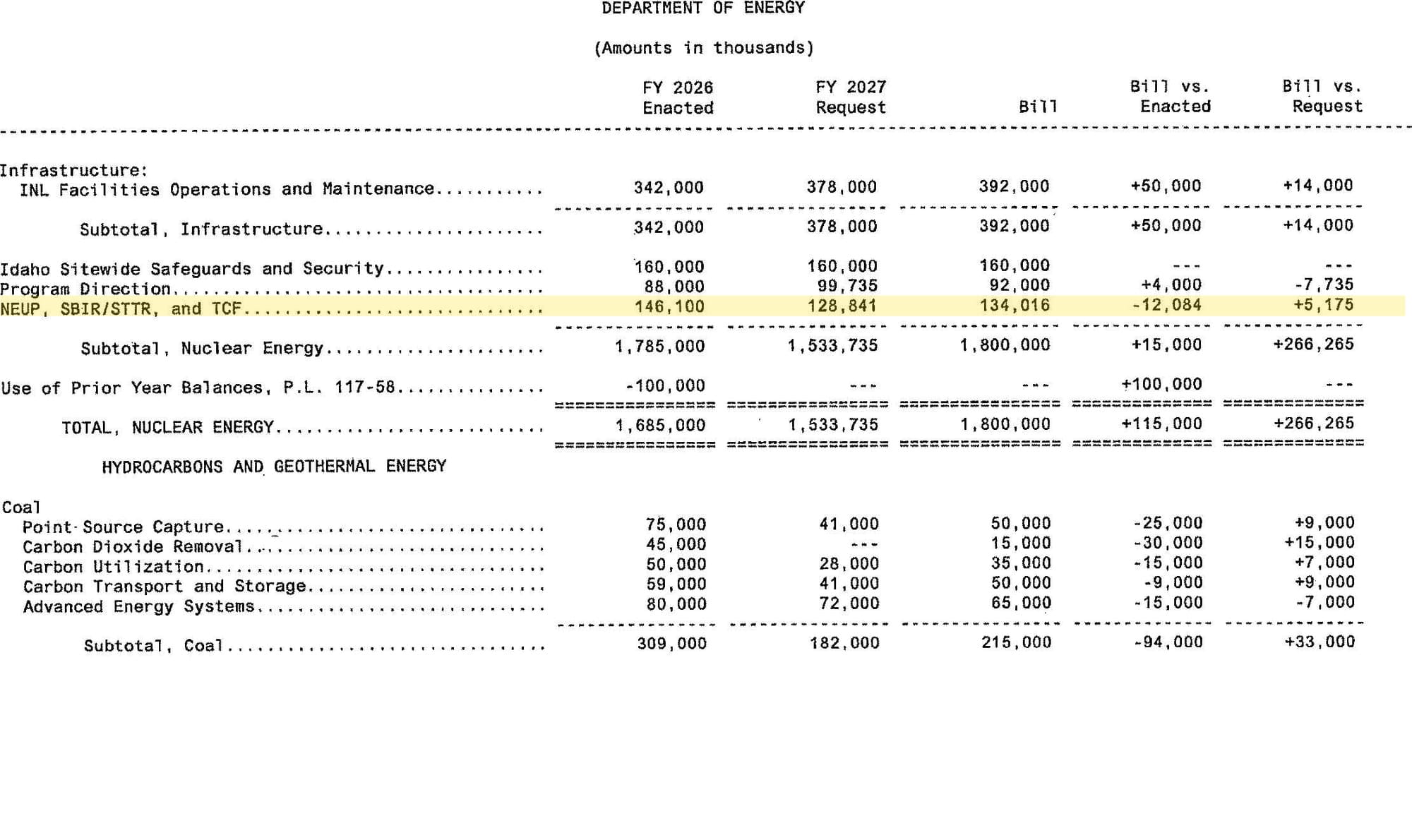

If you go to the Nuclear Energy section of the report, you'll see a table like the one below. This is an example of a detail table because they break the account total up into detailed subappropriations. It's 3 pages long, has many lines and surprise, surprise, adds to exactly $1.8 billion. Take a look:

On the last page, you see I've highlighted one line: NEUP, SBIR/STTR, and TCF. Let me translate. NEUP: Nuclear Energy University Program, SBIR/STTR: Small Business Innovation Research/Small Business Technology Transfer, TCF: Technology Commercialization Fund. So, while the statute says $360 million for NEUP, the appropriations act says NEUP, SBIR/STTR, and TCF together are $134 million.

Key insight: This is incorporation by reference, live. The report's funding table isn't just commentary here — the bill text deputizes one of its columns as binding law for that purpose. The number you'd find buried in the back of H. Rept. 119-667 is the number an appropriations lawyer would enforce. If you only read the bill, you literally cannot know what's available for the 954(a)(7) purpose — you have to go to the table.

5. Reconcile across the three documents.

- The CSBA shows the account total — $1.8 billion.

- The detailed "Department of Energy" table in the report breaks that total down by program, and its "Bill" column is what the proviso just made enforceable for the 954(a)(7) line.

- The bill text sets the ceiling and the carve-outs ($1.8B; $92M program direction).

Sometimes the topline masks a specific and particular disagreement between the Administration and the House mark. Sure, we know that the House and Administration are $266 million apart, but the detail table shows us that one program in particular — the Advanced Nuclear Fuel Availability Program — is nearly half of that $266 million delta, and most of the contention is in the larger Fuel Cycle Research and Development activity. You wouldn't know that unless you looked at the tables.

Pro Tip: Detail tables are like a CSBA but for a program. Not every account gets one, but most do. Like the CSBA, they live in the report, but aren't usually at the back with the CSBA, they're usually up with the account write-up in the report. It is just as vital a resource as the CSBA itself.

CRS' Appropriations Status Table: FY2027

The Catch: When Can You Actually Get It?

Here's the part that frustrates people who want the CSBA now.

The CSBA lives in the committee report. And the report isn't published when the bill is first taken up — there's a lag from subcommittee markup to when the report (and the CSBA) actually become available. In that gap, you're flying on the bill text plus whatever summary tables circulate. The CSBA is the moment the fog clears.

The timing differs by chamber:

- House: the report — and the CSBA — is generally available before full committee markup.

- Senate: the report comes after full committee.

That's exactly why H. Rept. 119-667 is worth flagging right now: the Energy & Water CSBA just became available. If you care where this bill is headed, this is the document to read today.

Pro Tip: If you're an open government data enthusiast, the House CSBAs will let you down. They are camera-ready copy, not traditionally typeset text. That means that the fine folks at GPO scan the printed CSBA pages into the report. In the machine-readable version of the report, the House CSBA spits out this absolute nightmare string:

Comparative Statement of Budget Authority

Pursuant to clause 3(c)(2) of rule XIII of the Rules of the House of Representatives, the following table provides a detailed summary, for each Department and agency, comparing the amounts recommended in the bill with amounts enacted for fiscal year 2026 and budget estimates presented for fiscal year 2027.

[GRAPHIC(S) NOT AVAILABLE IN TIFF FORMAT]

Womp, womp. That last line is the table. Every number you came for is locked inside a scanned image.

The Senate on the other hand, has GPO typeset their tables. Typesetting gets you a real machine-readable table. I concede it's not raw Markdown, JSON, or XML but it's infinitely better than a broken TIFF tag.

Why It Matters

For oversight and accountability, the CSBA is the chain-of-custody table — the first hard, account-level record of what Congress actually intends to do with the money. For agency budget shops, grantees, government affairs teams, and reporters, it's the fastest read on winners and losers in the bill: who got plussed up, who got cut, and who got told no.

This is what "follow the money" looks like in practice. The CSBA is the point where the money first becomes legible — before the floor, before conference, before the final enacted numbers. Read it early and you're not reacting to the bill. You're ahead of it.

Conclusion

One table. Five numbers per row. Two comparisons. Everything in thousands. Provisions you'd swear were free turn out to carry a price, and this is where you see it first.

Go to the back of the report before you read the front. The CSBA is the table the professionals live in — and now you can too.