Keeping Score: Who Referees an Appropriations Bill

The bill provides $58 billion. The allocation is $57.9 billion. Somebody has to decide whether that's a foul — and almost nobody reads the rulebook they're using.

The World Cup is nearing the end. Every goal that counted this tournament went through the same three things: an official scorer who keeps the tally, the Laws of the Game that says what counts as a goal and what you can and can't do in the process of getting one, and a referee willing to blow the whistle when somebody breaks the rules. Take away any one of them and the score on the board means nothing.

An appropriations bill works exactly the same way. There's an official scorekeeper. There's a rulebook for what counts as spending. And there's a mechanism to call the foul when a bill goes over the line. The trouble is that most people who follow appropriations — including a lot of people inside the process — have never read the rulebook and couldn't tell you who's keeping score.

Let's fix that. This is a post about scorekeeping: where it came from, who does it, what the score actually is, and how Congress enforces the number once it exists.

If you don't follow soccer: someone keeps the score, someone reviews the replay, and someone blows the whistle. That's the whole metaphor. You're covered.

The 60-Second Version

| Term | What It Is | Sports Analogy |

|---|---|---|

| Scorekeeping guidelines (OMB Circular A-11, Appendix A) | The agreed rules for what counts as budget authority and outlays, and when | The rulebook — what counts as a goal |

| House & Senate Budget Committees | The official scorekeepers — under §312, their numbers govern enforcement | The head referee (the chair), the recordkeeper, and the scoreboard operator |

| Congressional Budget Office (CBO) | Congress's nonpartisan estimator; produces the numbers the Committees rely on | The VAR and the linesman — reviews the play, flags the lines, advises the call |

| Cost estimate (§402) | CBO's price tag on an authorizing bill | The scouting report on a new signing |

| The appropriations score (§308) | CBO's tally of a spending bill's budget authority and outlays | The running scoreboard |

| 302(a) / 302(b) allocation | The ceiling the bill can't exceed | The salary cap |

| Point of order (§302(f), §311) | The objection that enforces the ceiling on the floor | The foul call |

Key insight: Congress doesn't enforce the topline by arguing about it. It enforces it with arithmetic — a number CBO produces, measured against an allocation Congress set for itself, and a Member willing to stand up on the floor and call the foul. No number, no scorekeeper, no whistle: no enforcement.

Translation: "How much does this bill spend?" is not a question of opinion. It has an official answer, produced by a specific office, under written rules. Everything in this post is about where that answer comes from and what happens when a bill exceeds it.

Why Anyone Keeps Score

To understand scorekeeping, you have to understand that for most of the 20th century, Congress didn't really do it — not in any disciplined, common way.

The machinery showed up in two waves.

1974 — the stadium gets built. The Congressional Budget and Impoundment Control Act of 1974 created the modern budget process: the annual budget resolution, the House and Senate Budget Committees, the 302 allocation system that divides the topline among committees, and a brand-new, nonpartisan number-cruncher to serve Congress — the Congressional Budget Office. Before CBO, Congress relied on the executive branch's numbers. After 1974, the legislature had its own scorekeeper (the Committees) and its own VAR and linesman (CBO).

1985 — everyone has to keep score the same way. The Balanced Budget and Emergency Deficit Control Act of 1985 — Gramm-Rudman-Hollings, P.L. 99-177, signed December 12, 1985 — was the first law that tried to put a hard, automatic constraint on the deficit. It set declining deficit targets aimed at a balanced budget by 1991, and if Congress missed a target, an automatic across-the-board cut called sequestration would do the cutting for them.

A law that triggers automatic cuts when a number is exceeded has a problem it absolutely must solve: everyone has to agree on the number. If OMB and CBO measure spending differently, the whole enforcement mechanism collapses into a fight about whose calculator is right.

So Gramm-Rudman-Hollings included a quiet, technical provision that turned out to be one of the most consequential sentences in federal budgeting. Section 252(d)(5) directed OMB and CBO to develop common scorekeeping guidelines, in consultation with the House and Senate Budget Committees.

Translation: 1974 gave Congress a scorekeeper and referee. 1985 made the legislative and the executive branch agree on the rules of the game. That agreement is the rulebook we're about to open.

(A footnote for the historians: Gramm-Rudman's automatic-cut mechanism got partially struck down by the Supreme Court in Bowsher v. Synar in 1986, was patched in 1987, and was effectively replaced by the discretionary spending caps and PAYGO of the Budget Enforcement Act of 1990. The deficit-target regime is long gone. The scorekeeping guidelines it spawned are very much still here.)

The Rulebook: A-11, Appendix A

That common rulebook lives in a place you'd never look for it: an appendix to an OMB circular.

OMB Circular A-11 is the rulebook for how the executive branch prepares and executes the budget. Tucked into the back, Appendix A is titled, plainly, Scorekeeping Guidelines.

It's the agreed-upon answer to questions like:

- When does budget authority count — when it's provided, or when it's spent?

- What's the difference between discretionary and mandatory spending, and who decides?

- How do you score a fee, a loan, an advance appropriation, a rescission?

- When a CHIMP (a Change In Mandatory Program) shows up inside an appropriations bill, how is it counted?

And while the application is complex and nuanced in practice, the guidelines are pretty terse. Sixteen principles, 5 pages.

The longest is purchase scoring rules (about a page) which also has a companion Appendix (Appendix B, 11 pages) on the budgetary treatment of leases and lease-purchases. But all in, 16 pages of text set the parameters for scorekeeping. Many are a single sentence, for example:

7. Advance appropriations

Advance appropriations of budget authority will be scored as new budget authority in the fiscal year in which the funds become newly available for obligation, not when the appropriations are enacted.

These aren't OMB's house rules. The guidelines were formally written down in 1997, in the joint explanatory statement accompanying the conference report for the Balanced Budget Act of 1997 (H. Rept. 105-217), and they've been revised since by agreement among "the scorekeepers" — CBO, OMB, and the Budget Committees. A-11 Appendix A is just where OMB publishes the current text.

Key insight: When people say a provision "scores" or "doesn't score," they're not being vague. They mean: under the Appendix A guidelines, does this provision or legislation produce a budgetary change impacting budget authority, outlays, or revenues? A policy can be a huge deal and score zero. A one-line technical change can score billions. The guidelines, not the rhetoric, decide.

Pro Tip: This is the single most useful document almost no one outside the process has read. If you've ever been baffled why a "cut" didn't reduce spending, or why a transfer that obviously moves money "doesn't count," the answer is almost always sitting in Appendix A. Read the current version here.

Pro Tip: All of these scorekeeping guidelines are built on an unwritten foundation: Score the doer. Some call this the "fingerprint test". If an appropriations bill changes an authorizing program, the appropriations committee bill gets the score. If an authorizing bill terminates an old program and rescinds funding for it, the authorizing bill gets scored. Recent reconciliation bills are a good example — billions of dollars for programs and accounts typically funded in an annual appropriations bill, charged to authorizing committees.

The Referee and the VAR: Committees and CBO

For Congress, the official scorekeepers are the Budget Committees. Think of a committee — really its chair — as the head referee, the official recordkeeper, and the operator running the scoreboard, all at once. They're assisted by the VAR and the linesman — the replay booth that reviews the tape and the official who flags what's out of bounds. That's the Congressional Budget Office: it reviews every play and hands up the number, but never makes the final call. (OMB keeps the executive branch's score; when the two diverge, the difference itself becomes a story.) CBO is nonpartisan by design and by fierce institutional habit — its job is to produce the number, not to like it.

But here's where it gets interesting, and where most people's mental model is wrong. CBO does not score every bill the same way. There are two completely different products, and the difference is the whole game.

Two Kinds of Score

1. The cost estimate (§402) — for authorizing bills. Under section 402 of the Congressional Budget Act, CBO is required to produce a formal written cost estimate for most bills reported by a committee. This is the famous "CBO score" you read about in the news: this bill will increase the deficit by $X billion over ten years. It's a scouting report — a projection of what a new policy will cost before it ever takes effect.

2. The appropriations score (§308) — for spending bills. Here's the twist almost nobody knows: appropriations bills are carved out of section 402. CBO is not required to produce a formal §402 cost estimate for a bill reported by the Appropriations Committees. Part of the origin of this split is historical. At the time the Congressional Budget Act was enacted, appropriations bills included lots of tables, charts, and figures — proto-scores, if you will.

Why? Because an appropriations bill doesn't project future costs — it is the cost. The number is right there in the bill. So instead, under section 308, CBO produces a different product: a tabulation of the bill's discretionary budget authority and outlays, account by account, including the budgetary effects of any CHIMPs riding along inside it.

That's not to say that CBO is taking a break during appropriations season. They work with the Appropriations Committees on all of the products included in the back of an appropriations report to comply with all of the budgetary points of order and chamber rules.

Translation: An authorizing bill gets a price tag — a guess about the future. An appropriations bill gets a scoreboard — a count of what's actually in it, measured against the limit it's allowed to hit. Same office, same rulebook, two very different jobs.

This §308 tabulation — the running scoreboard for a spending bill — is what people mean when they say "the appropriations score." And it's the tool that the Budget Committees use to do the enforcing.

Same Provision, Different Score: The Window

Here's where scorekeeping stops being bookkeeping and starts being strategy. The exact same words can score as a savings in one bill and a cost in another — not because anyone changed the policy, but because the two bills are measured over different windows under different rules.

Two things drive the difference:

1. The window. An appropriations score is essentially a one-year number — the discretionary budget authority you provide (or take back) this fiscal year, measured against the 302(b). An authorizing score runs the ten-year window (the budget year plus the nine that follow). That's not a small gap. Some effects are invisible in a one-year frame and enormous over ten.

2. What counts. By a scorekeeping convention formalized around 1990, the indirect revenue effects of discretionary appropriations generally aren't scored. The dollars are scored; the downstream consequences of spending them are not. Move the same dollars to the mandatory side and that revenue feedback comes roaring back in.

Translation: In an appropriations bill, you score the dollars in front of you, this year, and you stop. In an authorizing score, you look out a decade and you count the ripple effects. Same provision, two different questions — and sometimes two opposite answers.

The IRS Enforcement Example

The cleanest illustration in modern budgeting is IRS enforcement money, because enforcement spending makes money — every dollar of it collects more than a dollar in taxes already owed.

Now watch what happens to a single idea — rescind IRS enforcement funding — depending on where it sits.

On the appropriations side (one year, discretionary). You rescind, say, $1 billion of discretionary IRS enforcement appropriations. The score is clean: budget authority drops by $1 billion, outlays follow, and you book the savings. The taxes that won't get collected because the enforcement didn't happen? Not scored. The convention says the indirect revenue effects of discretionary appropriations don't count. A rescission here is pure savings.

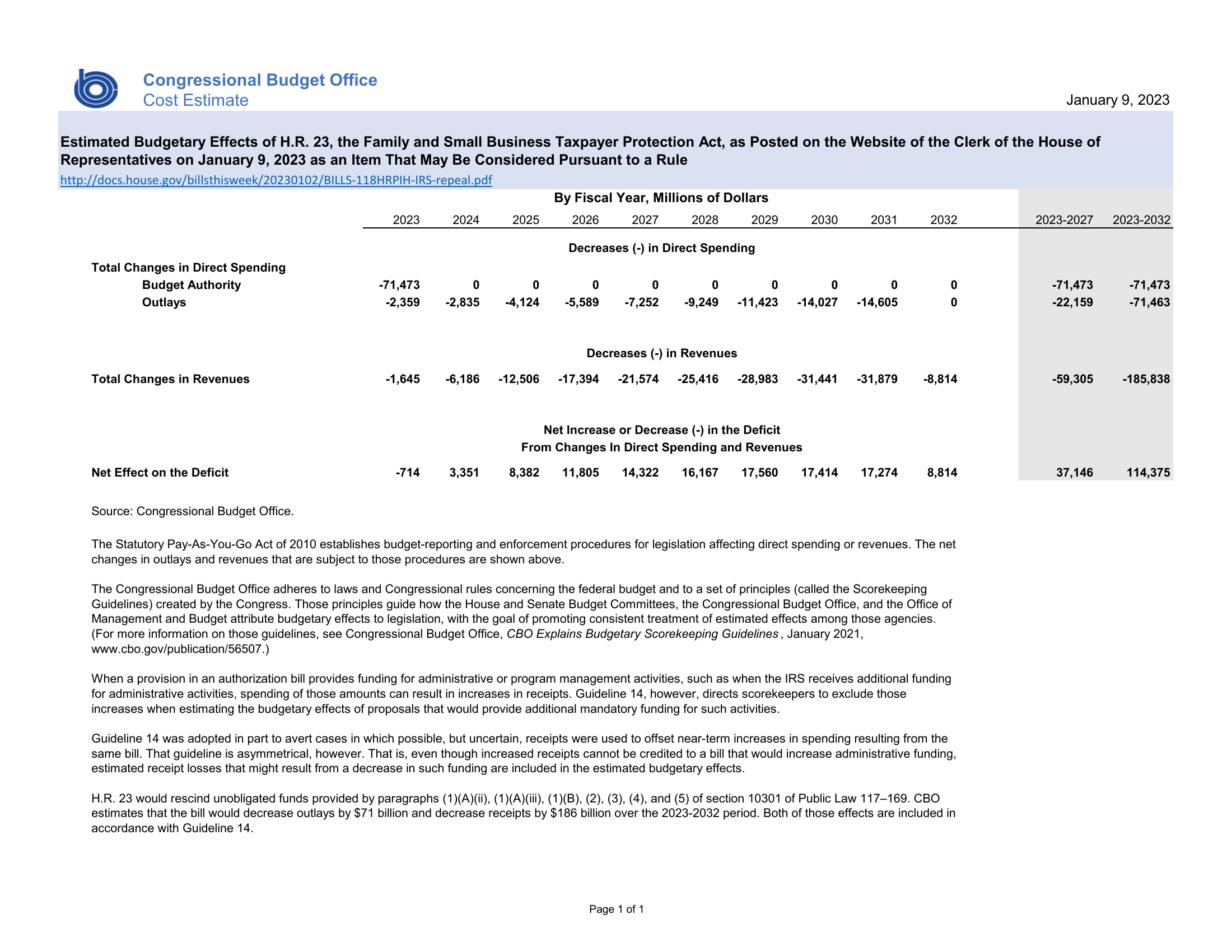

On the mandatory side (ten years, with feedback). Take the real case. The Inflation Reduction Act gave the IRS roughly $80 billion in mandatory funding. When the House moved to claw most of it back in H.R. 23 (118th Congress), CBO had to score it under PAYGO, over the full ten-year window, with the revenue feedback. The result stunned a lot of people:

Rescinding ~$71 billion of IRS funding would cut outlays by about $71 billion — but cut revenues by about $186 billion — for a net increase in the deficit of roughly $114 billion over 2023–2032.

A bill to cut the IRS scored as adding $114 billion to the deficit. Nobody changed a word of the underlying policy. The funding was mandatory, so the window was ten years and the forgone revenue counted. Likewise, a rescission of mandatory funding for the IRS would be estimated as a loss of revenues even if included as a Change in Mandatory Program (CHIMP) on an appropriations bill. Had those same enforcement dollars been a discretionary rescission of discretionary funds in an approps bill, the scoreboard would have read the opposite way: savings.

Source: CBO — Estimated Budgetary Effects of H.R. 23 | CBO — How Changes in Funding for the IRS Affect Revenues

Key insight: A provision doesn't have an intrinsic score. It has a score in a context — a window and a set of conventions. Before you accept that something "saves money" or "costs money," ask the two questions that decide it: over what window, and under whose rules? The same sentence can be a savings, a wash, or a $114 billion coster depending on the answers.

Pro Tip: This is why where you put a provision is a strategic decision, not a drafting accident. Move a policy between an appropriations bill and an authorizing vehicle and you can flip its score — which is exactly why fights over jurisdiction and vehicle are really fights over the scoreboard.

The Approps Score vs. the CSBA

If you've read our post on the CSBA — the Comparative Statement of (New) Budget Authority, the big account-by-account table in the back of every committee report — you might be thinking: isn't that the score?

No. And the distinction is worth getting exactly right, because it matters the moment anyone tries to enforce the number.

The CSBA is the Committee's table. It compares each account against the President's request and last year's enacted level, often in beautiful granular detail, sub-account by sub-account. It's the best single read on the policy story of the bill — winners, losers, what moved. We love the CSBA.

The CBO appropriations score is a different document with a different author and a different job. It's CBO's official §308 tabulation of the bill's budget authority and outlays, scored under the Appendix A guidelines and evaluated against the allocation the bill has to live within.

Here's the nuance that trips up even careful people:

The CSBA contains much of the information that's in the score — frequently in a more granular presentation. But it is not the score. If you were going to stand on the floor and assert a point of order that a bill breaches its allocation, you would need CBO's table, not the CSBA. And, more importantly, you need the Chair of the Budget Committee on your side, because the Budget Committee is the official.

Key insight: The CSBA tells you the policy story. The CBO score is the enforcement instrument. They overlap, they should reconcile, and they answer to two different entities — the Appropriations Committee versus the Budget Committee. When you need to prove a bill is over the line, only one of them counts.

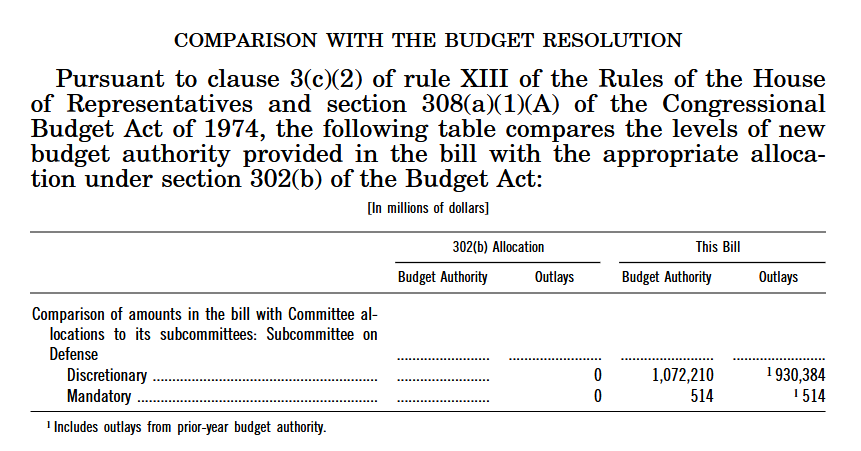

The Ceiling: 302(a) and 302(b)

A scoreboard is meaningless without a limit to measure against. That limit is the 302 allocation, and it comes down in two steps.

Section 302(a) — the topline gets divided. When Congress adopts a budget resolution, the total amount of budget authority and outlays in it gets allocated to each committee with spending jurisdiction. The Appropriations Committee gets the single biggest slice — the discretionary pie for the year.

Section 302(b) — the pie gets sliced. The Appropriations Committee then subdivides its 302(a) allocation among its twelve subcommittees — one number for Defense, one for Labor-HHS, one for Energy and Water, and so on. Those are the 302(b) suballocations, and that is the binding ceiling for each individual bill.

Translation: The 302(a) is the team's total salary cap. The 302(b) is how much the Appropriations Committee decides to spend on each position. When you hear that a bill is "over its 302(b)," it means the scoreboard (CBO's number) exceeds the cap the Committee set for that bill.

Key insight: The 302(b)s are where the real money fight happens, and they happen inside the Appropriations Committee, mostly out of public view. The topline is set by the budget resolution; the 302(b)s decide who at the table eats well and who goes hungry. Watch the 302(b)s and you know the priorities before a single bill hits the floor.

A note for the moment we're in: the statutory discretionary caps from the Budget Control Act of 2011 expired after FY2021, and the Fiscal Responsibility Act of 2023 set caps only for FY2024 and FY2025. With no statutory caps in force now, the 302(b) suballocation and the budgetary points of order are the live constraint on an appropriations bill. The scoreboard matters more, not less, when the automatic backstop is gone.

Calling the Foul: Points of Order

Here's the part that surprises people: the ceiling doesn't enforce itself.

A bill can exceed its allocation and sail right through — unless a Member stands up and objects. The objection is called a point of order, and it's the whistle in this whole system.

The two that matter most for appropriations:

- Section 302(f) — a point of order against considering a bill (or amendment) that would cause its committee allocation or subcommittee 302(b) suballocation to be exceeded. This is the bill-level foul: you're over your cap.

- Section 311(a) — a point of order against a measure that would breach the aggregate budget authority, outlay, or revenue levels in the budget resolution. This is the whole-budget foul: the league total is blown.

Three things make points of order behave less like a hard wall and more like a contested call:

- They're not self-enforcing. No Member raises it, no ruling happens, and the bill proceeds as if it were in bounds. The whistle only matters if someone blows it.

- The score is the evidence. To sustain a point of order that a bill breaches its 302(b), you need an authoritative number showing the breach — CBO's §308 score. This is exactly why the score-vs-CSBA distinction isn't academic. You bring CBO's table to that fight.

- They can be waived. In the House, the Rules Committee routinely waives budget points of order in the special rule for a bill, and notes known violations when assembling the rule. In the Senate, waiving most Budget Act points of order takes 60 votes. So the foul is real, but the game has a built-in way to play through it — if the votes are there.

Translation: A point of order isn't a force field. It's a right to object, backed by an official number, that the chamber can choose to honor or override. The constraint is real, but it's political, not automatic.

Why Should You Care?

"Is this bill actually over budget, or is that just spin?"

Don't take anyone's word for it. Find CBO's score for the bill and compare it to the published 302(b). The breach is arithmetic — and now you know which document holds the arithmetic.

"A program got 'cut' but spending didn't go down. How?"

Almost always a scorekeeping answer. Open A-11 Appendix A. The "cut" probably hit something that doesn't score — a transfer, a timing shift, a change that moves money without changing budget authority under the guidelines.

"Where's the real fight in this appropriations cycle?"

The 302(b) suballocations. They're set inside the Committee, they decide every bill's ceiling, and they're public once adopted. Read them before you read the bills.

"They're invoking a point of order — is the bill dead?"

Maybe not. Ask two questions: is there a number (CBO's score) that actually sustains the objection, and can it be waived (a House special rule, or 60 votes in the Senate)? The answer to both tells you whether the whistle stops play.

The Bottom Line

Key takeaways:

- Scorekeeping isn't bureaucratic trivia — it's the mechanism that turns "how much does this spend?" into an enforceable number.

- The rulebook is OMB Circular A-11, Appendix A — common guidelines that CBO, OMB, and the Budget Committees agreed to, traceable back to Gramm-Rudman-Hollings (§252(d)(5)) and written down in the 1997 BBA conference report.

- The officials are the House and Senate Budget Committees — under §312, their numbers govern enforcement (the chair is head referee, recordkeeper, and scoreboard all at once). CBO is the VAR and the linesman: it produces the estimates everyone relies on (hence "the CBO score"), but the official call is the Committee's.

- CBO does two jobs: a §402 cost estimate for authorizing bills (a forecast) and a §308 score for appropriations bills (a tally). Appropriations bills are carved out of §402 on purpose.

- The CSBA is not the score. It carries overlapping, often more granular numbers, but the enforcement instrument is CBO's §308 table. Bring the right document to the fight.

- The ceiling is the 302(a) allocation, sliced into 302(b) suballocations — the binding cap for each bill, and the real arena for the money fight.

- The whistle is the point of order (§302(f), §311). It's not self-enforcing, it needs CBO's number as evidence, and it can be waived. Real, but political.

Quick links: